Under The Hood, Wingstop Inc. ($WING)

COMPANY ANALYSIS & VALUATION

The author does not hold a position in Wingstop, Inc. at the time of publication. This report reflects the author’s personal views and is not investment advice. Investing carries the risk of permanent capital loss. Read full disclosure here.

1. The Business

Wingstop began franchising in 1997 and listed on NASDAQ in June 2015. As of the first quarter of 2026, the system operated 3,153 restaurants worldwide, of which 57 were company-owned. Approximately 98% of the system is owned and operated by independent franchisees who fund their own construction and equipment, typically an investment of approximately $580,000 per restaurant, and who bear the operating risk day to day.

Each restaurant occupies approximately 1,700 square feet of retail space, with no dining room and no drive-through. The format is designed entirely for order pickup and digital delivery. This small footprint keeps build-out costs predictable and accessible for franchisees, and enables the location density that the delivery model requires. When the majority of orders are placed through a digital platform for delivery, the restaurant closest to the customer captures the order. A 1,700 square foot location two miles away serves that customer more reliably than a larger format eight miles away.

Consolidated revenue of approximately $697 million in 2025 comes from three lines:

Royalty revenue, franchise fees, and other income totaled approximately $322 million, calculated as a percentage of franchisee sales with essentially no incremental cost to Wingstop. This is the highest-quality revenue line: it scales with the system rather than with anything Wingstop itself must build or staff.

Advertising fees totaled approximately $248 million, collected from franchisees and spent entirely on national marketing. This line passes through the income statement as both revenue and expense with no net contribution to operating income.

Company-owned restaurant sales totaled approximately $128 million, generated by the 57 locations Wingstop operates directly as testing grounds for new products, technology, and operational practices.

The technology infrastructure underpinning the system includes the proprietary ordering platform and mobile application, the Wingstop Smart Kitchen operating platform completed across all domestic restaurants in 2025, and the point-of-sale and restaurant management systems that franchisees are required to use. These are not the franchisee’s restaurant-level equipment. They are the shared digital backbone that makes the franchise operate as a single brand. The ordering data they generate feeds Club Wingstop, the national loyalty program launched in June 2026 following a pilot phase across 2025 and early 2026.

The domestic pipeline is entirely franchisee-driven. Every domestic development commitment as of December 2025 came from existing franchisees. These are operators who already run Wingstop restaurants, see their own cost structures, and continue to commit capital to additional locations. The strategy covers both existing markets, where density deepens brand presence and delivery coverage, and emerging markets where the brand is new. The long-term goal is to double the current domestic restaurant count, which implies expansion well beyond the markets where Wingstop currently operates. The pipeline committed to reach that target represents capital from franchisees who have seen enough in their existing stores to bet more.

Internationally, the system operated approximately 500 restaurants across 18 countries and U.S. territories as of early 2026, all franchised through master franchisee arrangements. The United Kingdom, under the ownership of Sixth Street Partners following the 2025 sale of Lemon Pepper Holdings, added more than 20 locations in 2025 and is the largest international market by restaurant count. India is planned for entry in 2026. Wingstop holds an 18.75% non-controlling equity stake in the UK entity following the sale of its larger prior position. International results are not broken out separately.

2. The Moat

Wingstop’s competitive advantage rests on a flavor-led brand with genuine cultural identity in the chicken wing category, and on the capital-light franchise structure that brand has enabled. These two things together, a brand that commands consistent consumer demand and a model that captures royalties from that demand without owning the infrastructure delivering it, are what makes Wingstop a structurally superior investment relative to a business that must own, staff, and maintain the restaurants it operates.

The Brand

Wingstop has spent thirty years building recognition in one specific product category. Twelve core flavors built around a flavor variety that no QSR format has replicated at the same depth. The brand competes on a specific eating experience. Cultural partnerships with musicians and athletes, and the 2024 designation as the official chicken partner of the NBA, have embedded the brand into sports and entertainment occasions in ways that persist through advertising cycles. A new entrant cannot acquire that positioning quickly.

The financial evidence for brand durability is in the pipeline. Existing franchisees, who see the full cost and revenue data for their own restaurants, are continuing to commit capital to new locations. In 2025, 100% of domestic development commitments came from existing operators. They are expanding into markets they already know with a product they have already proven. That behavior reflects genuine conviction in the brand’s ability to sustain demand, not compliance with a franchisor requirement.

The Capital-Light Model

The franchise structure is the source of Wingstop’s investment superiority. A company that collects royalties on approximately $5.3 billion in annual retail sales while deploying a corporate capital base of approximately $693 million in total assets is generating returns on capital that a restaurant operator bearing its own build-out costs and operating leverage could not approach.

ROIC averaged in the mid to high thirties for nine consecutive years against a WACC of approximately 11%. That 20-plus percentage point spread sustained across a decade is the direct financial expression of what it means to own the brand and the royalty right rather than the physical restaurants.

Each new restaurant a franchisee opens adds to the royalty income base at no capital cost to Wingstop. When same-store sales grow, royalty income grows proportionally on the existing base.

Saturating Markets as a Competitive Defense

The infill strategy that is currently compressing same-store sales at existing restaurants also builds a competitive barrier. When Wingstop reaches high density in a major market, it becomes significantly harder for a new chicken competitor to find viable real estate, build brand awareness from zero, and compete effectively against a system with multiple established locations, an active loyalty base, and a dominant delivery presence in the area. Wingstop’s management frames this explicitly as maximizing brand market share and visibility in key priority markets before extending into emerging ones. The short-term consequence is same-store sales redistribution. The long-term consequence is a market where a competitor would need to outspend and outoperate an already-entrenched network to gain a foothold.

Moat Assessment

The moat is strong. A competitor with sufficient capital and time could build a brand in the chicken wing category, but thirty years of single-category focus, genuine cultural recognition, and a franchise network of this scale create a lead that is meaningful and costly to close. ROIC at 32% in 2025 remains well above the cost of capital, the development pipeline is active, and no competitor has displaced the brand in its category. The same-store sales decline does not reflect a weakening of the competitive position. It reflects a deliberate expansion strategy adding delivery coverage in markets with proven demand, combined with temporary weather effects in Q1 2026.

3. Financial Performance

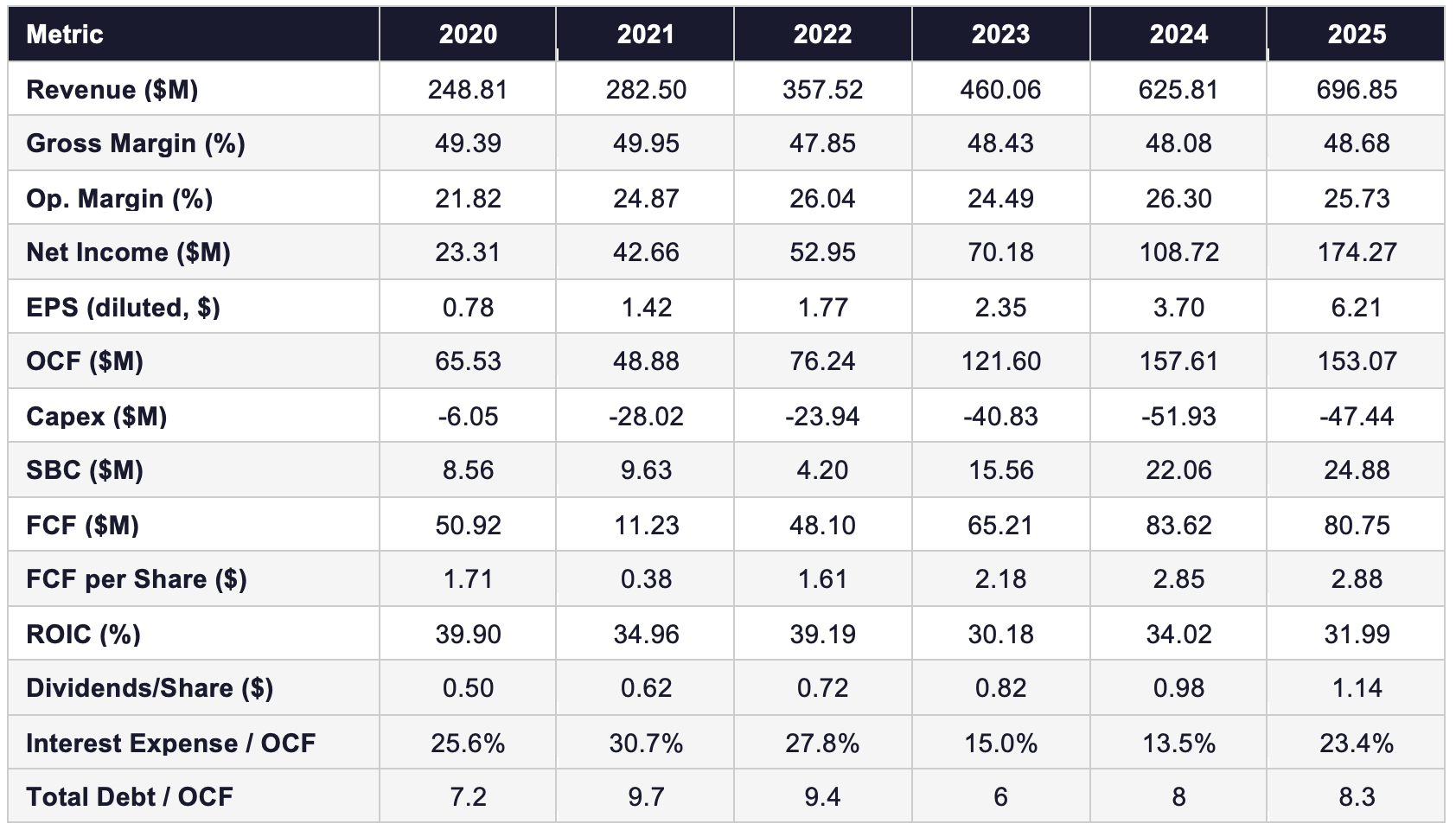

Total revenue grew from $248.8 million in fiscal 2020 to $696.9 million in fiscal 2025, a compound annual growth rate of approximately 23%. Royalty revenue, franchise fees, and other income grew from $108.9 million to $321.8 million, consistently representing between 43% and 46% of total revenue in every year. This is the only line that flows to Wingstop at essentially no incremental cost: it scales directly with system-wide sales and carries no operational overhead beyond the brand and technology infrastructure already in place. Advertising fees grew from $74.9 million to $247.6 million but pass through as both revenue and expense with no net contribution to operating income. Company-owned restaurant sales grew from $65.0 million to $127.5 million, representing approximately 20% of total revenue over the past five years. The count of company-owned restaurants grew from 32 at the end of fiscal 2020 to 57 at the end of fiscal 2025, representing approximately 2.4% of system-wide sales.

The 2025 net income figure of $174.3 million includes an $87.2 million gain on the sale of Wingstop’s UK equity stake, which inflated diluted EPS from a range of $0.78 to $3.70 between 2020 and 2024 to $6.21 in 2025. Adjusted EPS of $4.08, which excludes that gain alongside other non-recurring items, is the more accurate measure of what the underlying business produced. Adjusted EPS grew from $1.09 in 2020 to $4.08 in 2025, a compound annual growth rate of approximately 30%, running ahead of the 23% revenue CAGR over the same period. This outperformance reflects the starting point: net profit margin stood at 9.4% in 2020, a low base relative to the 13.7% average recorded in the five years prior and the 15.6% average in the four years that followed. The depressed starting amplified the adjusted EPS CAGR of approximately 30%.

Wingstop issues debt every other year through the securitized financing structure and distributes the proceeds to shareholders through dividends or share repurchases. In 2020, a $496 million issuance netted $162 million after repaying the prior tranche and was returned almost entirely as a special dividend of $163.8 million. In 2022, a $250 million issuance netted $247 million, of which $141.3 million was distributed as a special dividend. In 2024, a $500 million issuance netted $471 million, funding $314.7 million in share repurchases that year and leaving a cash balance that funded a further $221.9 million in repurchases in 2025. The buybacks reduced the diluted share count from approximately 29.8 million in 2020 to approximately 28.1 million in 2025, a reduction of 5.8%. Total debt to OCF ranged from 6.0 times at its tightest in 2023 to 9.7 times at its widest in 2021, and stood at approximately 8.3 times in 2025 following the $500 million 2024-1 issuance, which suggests it shall take Wingstop around 8.3 years to pay off its debt using its cash generated from its operations alone.

The interest burden is a direct consequence of the securitized debt structure, the proceeds of which are distributed to shareholders rather than retained in the business. Interest expense ranged from $14.9 million to $35.8 million, growing in line with each debt issuance. As a percentage of OCF, which ranged between $65.5 million and $157.6 million over the five-year period, interest consumed between 13.5% and 30.7%, moving with both the timing of each issuance and the level of OCF in any given year. In every year across the period, operating cash flow was sufficient to cover interest expense comfortably.

Capital expenditure was $6.1 million in 2020 and grew to a range of $24 to $52 million annually from 2021 onward, representing 7 to 10% of revenue. This capex does not build restaurants. Franchisees fund their own construction. Wingstop’s capex funds the shared digital infrastructure the entire franchise system runs on: the ordering platform, the Smart Kitchen operating system, the enterprise resource planning system, and the point-of-sale infrastructure across all domestic restaurants. This is largely growth capex rather than maintenance; however, as the major build phase completes and ongoing maintenance costs migrate from capital expenditure to operating expenses, the capex percentage should gradually moderate from current levels. The FCF margin moved from approximately 20.5% in 2020 to approximately 11.6% in 2025, compressing materially despite operating margin expansion, because elevated capex and growing SBC consume an increasing share of operating cash flow.

Q1 2026 Update

Domestic same-store sales fell 8.7% in the first quarter of 2026 against a decline of 0.5% in the same period a year earlier. On the Q1 2026 earnings call, CEO Michael Skipworth stated that atypical winter weather resulted in temporary closures across over 700 domestic restaurants during the quarter, concentrated in the Midwest and Northeast where the franchise network is densely penetrated. Management attributed approximately 4 percentage points of the decline to those disruptions. The 8.7% figure covers the entire domestic system. Company-owned restaurants within that system declined only 2.2%, reflecting their concentration in Texas markets that largely avoided the most severe weather. The gap illustrates how heavily the impact was concentrated in the franchised network’s Midwest and Northeast footprint.

Adjusting for weather, the underlying same-store sales trend is negative by roughly 4 to 5 percentage points. A portion of that residual reflects the hard comparison against 19.9% growth in fiscal 2024. The remainder reflects the infill strategy: new restaurants opening in the same markets as existing ones, capturing delivery occasions from nearby locations and reducing those locations’ same-store sales in the process. The existing restaurant loses some transactions to the new one next door, but the franchisee who owns both sees their total portfolio revenue grow. System-wide sales, which count every restaurant, grew 5.9% to approximately $1.4 billion in the quarter, confirming that total demand through the system continued expanding even as the per-store metric contracted. Zero permanent domestic restaurant closures were recorded. Ninety-seven net new restaurants opened.

4. Capital Allocation

Wingstop is a capital-light business by design. Franchisees fund the construction and operation of every restaurant. The company itself deploys capital through three channels: dividends, technology infrastructure investment, and share repurchases.

The dividend has grown annually since its introduction in 2017, reaching $1.14 per share in 2025. At the current price this yields approximately 0.8%, with a payout ratio of approximately 28% of adjusted net income, adjusted for the UK equity stake gain and other non-recurring items. Dividends are paid out of the recurring royalty cash flows the business generates, with special dividends distributed amidst the debt issuance.

The buyback program is funded not from organic free cash flow but from the proceeds of debt issuances. Wingstop borrows against its royalty cash flows through the securitized financing structure and uses the proceeds to retire shares. Three authorizations have run since August 2023: an original $250 million program, an additional $500 million in December 2024, and a further $300 million in March 2026. Across all repurchases through Q1 2026, the company retired approximately 2.96 million shares at a blended average price of approximately $252.

Capital expenditure, has run between 6.7% and 11.3% of revenue in every year since 2019. It covers the shared digital infrastructure described in the Financial Performance section and does not fund restaurant construction, which is the franchisee’s cost.

5. Competition

Wingstop is the largest chicken wing-focused restaurant chain in the world by location count. The wing category has several direct competitors, all of which compete primarily on occasion rather than on the same digitally-native, delivery-first, small-footprint franchise model Wingstop operates.

Buffalo Wild Wings

Buffalo Wild Wings operates approximately 1,600 locations in the United States and is the most visible brand associated with the chicken wing occasion. The format is fundamentally different: larger footprint, full-service bar, dine-in oriented, and heavily tied to the sports bar occasion. Buffalo Wild Wings has been owned by Inspire Brands since 2018 and does not report separately. The dining format means it competes for the same wing consumer on a different occasion type, the planned in-venue sports viewing experience rather than the everyday delivery order. Wingstop’s digital-first delivery model largely avoids that direct occasion comparison.

Chicken Category Competitors

KFC operates more than 25,000 locations globally across dine-in and drive-thru formats, owned by Yum Brands. It competes on a full chicken menu at a broad price range and targets a different consumer occasion entirely: a planned, family-style meal rather than a digital delivery wing order. The scale comparison is instructive for understanding Wingstop’s long-term runway, but the format, occasion, and ownership model share little with Wingstop’s delivery-first franchise structure.

Popeyes is the most operationally comparable publicly observable franchise by product category: chicken-focused, predominantly franchised, and reporting same-store sales through Restaurant Brands International. Popeyes comparable sales declined 6.5% in Q1 2026, against a decline of 4.0% in Q1 2025, a result its management described as among the weakest in roughly 20 years. The surface parallel with Wingstop’s 8.7% decline does not hold under examination. Popeyes grew its restaurant count at only 1.2% net in Q1 2026, with system-wide sales declining 3.9% as a result. Wingstop, by contrast, opened 97 net new restaurants in the same quarter with system-wide sales growing 5.9%. Wingstop’s SSS decline at existing locations reflects demand being redistributed to nearby delivery hubs that the same franchisee owns, a deliberate and self-funded consequence of the infill strategy. Popeyes does not operate the same delivery-first, small-footprint densification model. Its SSS decline reflects competitive pressure on a relatively static store base. The two numbers look similar. The business logic behind them is different.

Third-Party Delivery Platforms

Approximately 73% of Wingstop’s system-wide sales flow through digital channels, with a meaningful portion through third-party delivery platforms at commission rates typically in the 15 to 30% range. Wingstop earns its royalty on gross sales regardless of channel. The commission cost sits entirely with the franchisee. A restaurant generating significant volume through aggregators at a 25% average commission rate is absorbing a material cost that reduces the net economics of each order but does not appear in Wingstop’s own income statement. This is a structural cost at the franchisee level that must be held in mind when reading system-wide sales growth as a measure of franchisee profitability.

6. Management

Michael J. Skipworth, President and Chief Executive Officer

Michael Skipworth joined Wingstop in December 2014 and progressed through finance and operations roles, including CFO and Chief Operating Officer, before being appointed President and CEO in March 2022. He has been present for the digital platform build-out, the international expansion, and the current same-store sales cycle.

His standard annual compensation comprises a base salary of $1,000,000 and a performance-based cash incentive with a target of $1,200,000 weighted 80% to adjusted EBITDA growth and 20% to net new unit openings. In 2025, the company opened 493 net new units against a maximum bonus threshold of 360, exceeding the ceiling by 37%. The annual cash incentive paid at 142% of target. The unit opening metric creates a direct link between management’s annual compensation and the infill strategy that simultaneously drives same-store sales lower at existing locations. The independent check on whether the strategy is commercially justified, rather than compensation-driven, is franchisee behavior: existing operators committing voluntary capital to new locations in the same markets at double-digit annual rates.

Total 2025 compensation was approximately $35.3 million, elevated by a retention award of approximately $25 million approved in September 2025. The award comprises $12.5 million in service-based RSUs with a five-year cliff and no performance condition, and $12.5 million in performance-based units measured against system-wide sales targets from Q3 2029 through Q2 2030. Half the award is guaranteed by continued employment alone. The deliberation ran from April through September 2025, a period during which the same-store sales deterioration was already visible.

Skipworth’s personal beneficial ownership stands at approximately 44,100 shares, worth approximately $6.3 million at current prices. The four largest institutional holders are BlackRock at approximately 9.96%, T. Rowe Price at approximately 7.83%, Lone Pine Capital at approximately 5.43%, and Massachusetts Financial Services at approximately 5.12%. There is no founder stake and no controlling shareholder.

7. Growth Levers & Addressable Market

The Infill Strategy: Why Franchisees Are Expanding in Existing Markets

The domestic expansion strategy concentrates new openings in markets the system already serves before extending into new geographies. This is not an accident of franchisee preference. It is a deliberate commercial rationale built into the economics of the model.

When a new Wingstop opens in a city where the brand already operates and advertises, the advertising fund is already covering that market. The new restaurant pays into the fund and immediately benefits from existing brand awareness at no incremental marketing investment from Wingstop or the opening franchisee beyond what the fund already commits. In a new geography, building brand recognition requires months of local marketing investment before the first regular customer develops a habit. The financial model for an infill restaurant is therefore more predictable and less capital-intensive in marketing terms than a greenfield entry.

Supply chain efficiency reinforces this. All food and packaging for domestic restaurants flows through a single national distributor with 23 geographically diverse distribution centers. Clustering restaurants in existing markets reduces last-mile delivery costs, improves freshness, and simplifies logistics.

The delivery format makes density a functional requirement. Wingstop’s 1,700 square foot restaurant serves a realistic delivery radius of roughly three to five miles at acceptable delivery times. A major metropolitan area requires multiple locations to achieve the coverage needed to serve every delivery zone within a reasonable window.

Existing franchisees are the ones driving this expansion because they see it working in their own portfolio. An operator who owns one restaurant and opens a second two miles away may see the original store’s same-store sales decline by 5 to 8%, but their total portfolio revenue grows substantially if the new restaurant reaches even 70 to 80% of the original’s AUV. The combined economics of the expanded portfolio are what franchisees are optimizing, not the per-store metric. Their continued commitment to opening at double-digit rates, in markets they already know and where they are already invested, is the clearest available signal that the combined portfolio economics justify the expansion.

The Path to 10,000 Restaurants

The domestic pipeline is pointed at a long-term goal that requires substantial geographic expansion beyond current markets. The company has stated it can double the domestic restaurant count from approximately 2,650 to over 5,000 through both existing and emerging markets. At an annual unit growth rate of 15 to 16%, the domestic system would reach approximately 5,000 restaurants within roughly seven years. Reaching the company’s broader stated ambition of more than 10,000 total restaurants worldwide requires both the full domestic buildout and continued international expansion across markets where Wingstop is still early.

The committed domestic pipeline already represents the foundational layer of this growth. Development agreements signed by existing franchisees commit them to specific opening schedules across specific markets. When 100% of those commitments come from existing operators, it reflects franchisees who have already operated in the system, verified the unit economics in practice, and made a forward commitment to expand further. This is not speculative demand from untested franchisees. It is contracted growth from proven operators.

International Runway

The system operated approximately 500 international restaurants across 18 countries and U.S. territories as of early 2026. The United Kingdom added more than 20 locations in 2025. India is planned for entry in 2026. The 1,700 square foot format, requiring no dining room, minimal staffing relative to a full-service restaurant, and compatible with any cuisine culture that accepts chicken as a protein, travels well across international markets. The master franchisee structure concentrates local market knowledge in a partner who assumes the development risk, limiting Wingstop’s direct capital exposure to international growth. International results are not separately disclosed.

8. Valuation

The future return on Wingstop stock is a function of two engines: the future growth in free cash flow per share and any valuation re-rating. Both are explained below.

Free cash flow throughout this report is operating cash flow less capital expenditure less stock-based compensation.

Engine 1: Fundamentals

The first engine is the business itself. FCF per share grows over time through revenue expansion, operating leverage, and share count reduction from buybacks. That growth, compounded annually, is what the fundamental engine delivers regardless of any valuation re-rating.

For Wingstop, the primary driver is unit growth compounding royalty income on a growing system-wide sales base. At 15 to 16% annual net new restaurant openings, system-wide sales grow even when same-store sales are flat or modestly negative. Each new restaurant adds to the royalty income base at no capital cost to Wingstop. Buybacks add per-share amplification effect as the diluted share count declines.

Engine 2: Valuation Re-Rating

At today’s price of approximately $166, the investor is paying for everything this business will earn over roughly the next 23 years, in today’s money. Everything it earns beyond that point comes to the investor at no additional cost. The fewer the embedded years, the more of the future the investor receives without paying for it.

At 23 embedded years, the price is not offering an investor a meaningful valuation tailwind. The fundamental engine is doing the work here: unit growth compounding royalty income on a growing system-wide sales base, with same-store sales expected to normalize as the hard prior year comparison fades, weather effects clear, and new restaurants mature into the same-store calculation. That engine is sufficient on its own to generate a reasonable return from this price.

However, it is worth mentioning that Capital-light franchise businesses with this degree of cash flow predictability have historically traded at a persistent premium to the broader market, which suggests the valuation here carries less downside risk than the embedded years figure alone would imply for a typical business.

For a detailed explanation of how this valuation framework works, please read A Comprehensive Guide to Business Valuation.

9. Risks

Same-Store Sales Normalization Timeline

The 8.7% domestic same-store sales decline in Q1 2026 reflects several identifiable components. Management attributed approximately 4 percentage points to weather-related temporary closures in Midwest and Northeast markets. A meaningful portion reflects the hard comparison against 19.9% growth in fiscal 2024, which fades progressively over the next four quarters. And a portion reflects the natural redistribution of demand within markets where the infill strategy has added new locations near existing ones.

The first two effects ease or resolve without any change in business strategy. The fourth resolves as new restaurants mature past their first year and enter the same-store calculation as contributors, and as the infill strategy progressively pivots toward new geographic markets where the redistribution dynamic does not apply. The risk is the timeline: if the normalization takes longer than expected, or if the hard comparison is followed by category-level demand softness, same-store sales could remain negative beyond the period explained by known transient factors.

Product Economics and Value Competition

Bone-in chicken wings cannot be restructured to hit a sub-$10 price point without reducing wing count below the threshold that makes the order satisfying. The average Wingstop ticket runs above $20. At that price, a consumer recalculating food spend compares Wingstop against cheaper alternatives: a burger, a pizza, or a home-cooked meal. Wingstop cannot build a value floor the way a burger operator can engineer a $5 meal around inexpensive protein. When consumer budgets tighten, ordering frequency at premium-ticket formats falls first. This is a structural feature of the product category that has always existed and will persist regardless of what management does.

Bone-in wings also carry no meaningful commodity hedge. There are no established fixed-price markets for fresh bone-in chicken, which accounted for approximately 20.5% of company-owned restaurant cost of sales in 2025. The 2019 episode, when COGS grew 53.8% against 30.4% revenue growth as wing prices spiked, established the precedent for how quickly input cost pressure translates into restaurant-level margin compression. If chicken wing costs rise during a period of same-store sales pressure, franchisee margins compress from both revenue and cost simultaneously.

10. The Verdict

The business has demonstrated through a decade of operation that its franchise model generates exceptional returns on a minimal corporate capital base. ROIC averaging in the mid to high thirties against a WACC of approximately 11%, sustained across a full decade that included a pandemic, a commodity cost event, and the same-store sales decline now dominating the stock’s narrative. A brand with thirty years of category identity in chicken wings that no competitor has displaced. A system that grew from approximately $2.7 billion to approximately $5.3 billion in system-wide sales in four years on capital deployed overwhelmingly by franchisees rather than by the company. These are the financial expressions of a model that earns the Approved designation.

Domestic same-store sales have been negative for five consecutive quarters. System-wide sales have grown in every one of those quarters. The two facts coexist because same-store sales measures only mature, existing restaurants, while system-wide sales counts everything. When a new restaurant opens near an existing one and serves customers who were previously too far for a reasonable delivery, the existing restaurant’s same-store metric declines and the system’s total sales grow. That is not brand deterioration. That is the delivery-focused franchise model expanding its physical coverage in markets where the brand has already demonstrated demand.

The franchisees make this case more compelling than any financial metric. Every domestic development commitment in 2025 came from existing operators who see the full cost and revenue data for their own restaurants. They are expanding into adjacent delivery zones in markets they already serve, committing their own capital at double-digit annual rates, because the combined economics of their growing portfolio justify the investment. Franchisees who believed the economics were broken would not be doing this. They are.

The risks are real and stated plainly. The product economics of bone-in wings do not allow Wingstop to match the value floor available to burger or pizza operators, which creates exposure to consumer spending pressure that is structural, not cyclical. The compensation structure links management’s cash incentive to unit openings in a way that warrants monitoring. None of these individually or collectively changes the Approved designation. They are costs to the return on a business whose model continues to compound.

The author does not hold a position in Wingstop, Inc. at the time of publication. This report reflects the author’s personal views and is not investment advice. Investing carries the risk of permanent capital loss. Read full disclosure here.