Under The Hood, Universal Health Services - $UHS

Deep Analysis & Valuation

The Outlook

More than 1 in 4 American adults lives with a mental illness or substance use disorder, according to the Substance Abuse and Mental Health Services Administration. The infrastructure available to treat them has never kept pace with that need; behavioral health has historically attracted less capital, lower reimbursement, and less institutional attention than any other major category of inpatient care. Universal Health Services has been building inside that gap since 1979, when Alan B. Miller founded the company in a single acute care hospital in King of Prussia, Pennsylvania. Today it operates one of the largest behavioral health networks in the world; 346 inpatient facilities across the United States, the United Kingdom, and Puerto Rico, alongside 29 acute care hospitals and 35 freestanding emergency departments.

The regulatory environment introduces real pressure. The One Big Beautiful Bill Act, enacted July 4, 2025, is expected to reduce UHS’s aggregate annual net benefit from Medicaid supplemental payment programs by $432 million to $480 million by 2032, phasing in gradually from 2028 on a pro rata basis. Those programs generated $1.339 billion in net benefit in 2025 alone, representing approximately 67% of consolidated operating income that year. The pressure extends beyond the supplemental reduction: Medicaid work requirements and the expiration of ACA premium tax credits are simultaneously shifting patients from insured to uninsured status. Management has runway to offset the headwind through volume growth, pricing discipline, and operational improvement, but the trajectory warrants close attention. What partially offsets this picture is the balance sheet; total debt of $5.2 billion against operating cash flow of $1.864 billion puts the leverage ratio at approximately 2.8 times, structurally cleaner than most for-profit hospital peers. The founder’s family retains majority voting control through a dual class share structure, a concentration of decision-making authority that has historically favored consistent capital allocation over short-term market appeasement.

Key Terms

Acute Care Hospital

A facility providing short-term medical treatment for severe injuries, illnesses, and surgical procedures requiring continuous clinical oversight. UHS operates 29 inpatient acute care hospitals, supplemented by 35 freestanding emergency departments and 13 outpatient centers. The acute care segment generated approximately 57% of UHS’s consolidated revenues in fiscal year 2025.

Behavioral Health

Inpatient and outpatient services treating psychiatric conditions, substance use disorders, and related conditions. UHS’s behavioral health segment encompasses 346 inpatient facilities across the United States, United Kingdom, and Puerto Rico, together with 119 outpatient locations. Revenue from behavioral health represented 43% of consolidated revenues in fiscal year 2025.

Same-Facility Metrics

Financial and operational results calculated only for facilities that operated in both the current and prior year period, eliminating distortions caused by new openings, acquisitions, or closures. UHS discloses same-facility revenue growth, admissions, and revenue per admission separately or each segment. Same-facility data is the most analytically useful measure of organic operating performance.

Revenue Per Adjusted Admission

A measure of revenue generated per patient visit, adjusted to incorporate outpatient volume on a standardized basis. When revenue per admission rises without a corresponding increase in admissions, it reflects pricing power, payer mix improvement, or acuity shift rather than volume. In the first quarter of 2026, UHS reported revenue per admission growth of 6.3% in acute care and 6.2% in behavioral health on a same-facility basis.

One Big Beautiful Bill Act (OBBBA)

Federal legislation enacted July 4, 2025, that restructures several healthcare financing mechanisms with direct implications for hospital operators. The Act imposes a gradual reduction in the provider tax rates that states may use to fund Medicaid supplemental payment programs, capping the mechanism that has historically allowed states to generate federal matching funds above standard Medicaid base rates. It also introduces work and community service requirements for certain Medicaid beneficiaries and eliminates the enhanced premium tax credits that subsidised ACA exchange-based insurance for lower income Americans. The combined effect of these three provisions is a reduction in both the supplemental payment net benefit hospitals receive and the size of the insured patient population. The Act phases in its most significant provisions beginning with the 2028 state fiscal years.

ACA Exchange

A government-run online marketplace where individuals purchase private health insurance plans from competing insurers. Exchange-based insurance is distinct from employer-sponsored coverage, Medicaid, and Medicare. Lower income individuals who purchased exchange plans were eligible for federal premium tax credits that subsidised their monthly premiums. The expiration of enhanced premium tax credits at year-end 2025 made exchange plans unaffordable for many enrollees, converting previously insured patients to uninsured status. Exchange admissions at UHS declined approximately 15% in the first quarter of 2026 while uninsured admissions increased approximately 16%.

Medicaid Supplemental Payment Programs (SDPs)

State-directed Medicaid arrangements that compensate hospitals at rates above standard fee-for-service, funded jointly by states and the federal government. These programs, which vary by structure and state, contributed $1.339 billion in aggregate net benefit to UHS in fiscal year 2025. The One Big Beautiful Bill Act restricts the future structure of these programs, capping payments at Medicare rates for newly established programs and imposing reductions on grandfathered programs beginning in 2028.

Medicaid Managed Care

A system in which states contract with private health plans to administer Medicaid benefits on their behalf. Managed Medicaid plans pay rates negotiated with providers, which may differ materially from standard Medicaid fee-for-service rates. Approximately 42% of UHS’s behavioral health revenues come from Medicaid and managed Medicaid combined; the acute care segment’s comparable exposure is approximately 20%.

Certificate of Need (CON)

A regulatory requirement in many states compelling healthcare providers to obtain state approval before constructing new facilities, adding licensed beds, or expanding services. CON laws create a structural barrier to competitive entry in regulated markets, protecting the revenue base of established providers like UHS.

Return on Invested Capital (ROIC)

A measure of how efficiently a business generates operating profit from its deployed capital base. We here compute ROIC as NOPAT, net operating profit after tax, divided by invested capital, defined as total assets less goodwill, accrued liabilities, and cash. This methodology isolates operational efficiency by removing acquisition premiums, supplier financing, and non-operational assets from the capital base, measuring the return generated by the operating assets of the business rather than the accounting residual after financing decisions. ROIC figures will therefore differ from those published by standard financial data providers.

At a Glance

Company: Universal Health Services, Inc.

Ticker: $UHS · NYSE

Sector: Healthcare

Industry: Hospital Operations & Health Services

Market Capitalization: ~$8.8 billion (at $146)

First Coverage: June 2026

FY2025 Revenue: $17.365 billion

Disclosure: The author holds a position in Universal Health Services, Inc. This report reflects the author’s personal views and is not investment advice. Investing carries the risk of permanent capital loss. Read the full disclaimer here.

1. The Business

Alan B. Miller founded Universal Health Services in 1979, the day after his previous company was acquired in a hostile takeover. He had built American Medicorp into the second largest hospital management firm in the United States before losing it, and he structured UHS from the outset so that it could never happen again; the publicly traded share class was designed to carry the majority of economic equity but minimal voting power, concentrating control permanently in management’s hands. That structure remains intact today, with Alan B. Miller serving as Executive Chairman and his son Marc D. Miller serving as Chief Executive Officer since January 2021. What began with six employees and zero revenue is today a Fortune 500 company generating $17.365 billion in annual revenues and employing approximately 101,500 people across 40 states, the United Kingdom, and Puerto Rico.

What the Company Does

UHS owns and operates acute care hospitals and behavioral health facilities through its subsidiaries. Acute care hospitals treat patients with immediate or urgent medical needs; emergency presentations, surgical procedures, cardiac events, and obstetrics. The patient receives treatment over an average inpatient stay of approximately 4.8 days, and is discharged.

Behavioral health facilities treat patients with psychiatric conditions, substance use disorders, and related diagnoses. Average length of stay at UHS behavioral health facilities was 13.7 days in 2025, nearly three times the acute care average. The cost structure is predominantly labor rather than equipment and supplies, and revenue is driven by daily census rather than procedure volume.

Geographic Concentration

UHS organizes its acute care operations primarily across Sun Belt states with above-average population growth. Texas and Nevada together contributed approximately 33% of consolidated revenues in 2025, with California contributing a further 11%. Texas and Nevada are also the two states where UHS generates its largest Medicaid supplemental payment program benefits, making the geographic concentration analytically significant for both the revenue growth story and the regulatory risk discussion. The behavioral health division operates across a substantially broader geography, with 182 US inpatient facilities spanning 40 states and the District of Columbia. The United Kingdom operations, comprising 161 inpatient behavioral health facilities, generated approximately $1.001 billion in revenues in 2025 under contracts with the National Health Service and other local government bodies.

Revenue Mix

UHS derives its revenues from four primary payer categories. Managed care and private insurers account for approximately 28% of consolidated revenues. Medicare accounts for approximately 11%, with managed Medicare adding a further 12%. Medicaid accounts for approximately 15%, with managed Medicaid adding 14%. Together, government programs account for approximately 52% of consolidated revenues. The payer mix diverges materially between segments. Managed care accounts for approximately 33% of acute care revenues, giving that segment meaningful commercial pricing leverage. In behavioral health, Medicaid and managed Medicaid together account for approximately 42% of segment revenues, reflecting the patient population this segment serves. Serious mental illness and substance use disorders disproportionately affect lower-income populations covered by Medicaid, making the behavioral health segment structurally more dependent on government reimbursement than acute care.

Medicaid Supplemental Payment Programs

Embedded within the Medicaid revenue line an analytically important revenue layer: state-directed supplemental payment programs that compensate UHS above standard Medicaid base rates. These programs, which vary by state and require periodic reapproval, generated $1.339 billion in aggregate net benefit to UHS in 2025. Federal legislation enacted on July 4, 2025, restricts the future structure of these programs, with management estimating that the aggregate annual net benefit will be reduced by $432 million to $480 million by 2032. The supplemental payment layer is an essential component of the current business model, not a peripheral benefit. It is legislatively contingent and now in mandated decline. At current levels it is the primary driver of reported consolidated profitability, and its gradual reduction is what the trajectory of this business must be measured against.

2. The Moat

UHS’s competitive advantage is the structural economics of its behavioral health platform: a category with low capital intensity, recurring length-of-stay revenue, and a referral network built over 47 years.

Structural Economics of Behavioral Health

Behavioral health inpatient facilities do not require the physical infrastructure that defines acute care hospitals. There are no surgical theaters, no imaging suites, no intensive care units demanding continuous capital replacement. The dominant cost is labor. Revenue is generated by daily census across an average length of stay of 13.7 days rather than by episodic high-cost procedures. That combination produces a cost structure that is predictable in its composition and generates margins that acute care cannot match.

The financial proof is in the consistency. Same-facility behavioral health operating margins were 20.5% in 2025 and 20.3% in 2024, held across a period of labor inflation, reimbursement uncertainty, and an active federal legislative headwind. Acute care margins over the same period were 12.1% and 10.0% respectively. The 850-basis point differential between the two segments is a structural feature of the behavioral health business model that has persisted across multiple reimbursement cycles. A business whose margins hold in a narrow band through those conditions while simultaneously growing same-facility revenues at 7.7% is demonstrating structural pricing power.

Referral Network Density

Psychiatric patients do not self-refer. They arrive through primary care physicians, emergency rooms, schools, court systems, and other hospitals. A referral source needs to know a qualified bed is available and that the facility has the clinical capability to treat the patient’s specific condition. UHS’s national footprint of 182 US inpatient facilities across 40 states, with approximately 24,200 available behavioral health beds, means that referral sources across a wide geography can direct patients to a UHS facility with a level of reliability that a regional operator cannot match.

The shortage of inpatient behavioral health beds in the United States is structural and chronic. Patients requiring the highest-acuity placements, those who are hardest to place and who generate the highest revenue per day, flow toward networks with proven capacity and clinical breadth. UHS’s four-decade presence across 40 states positions it to capture that flow in a way that a newer or more geographically concentrated operator cannot replicate without years of facility construction and relationship building. Certificate of Need (CON) laws in most states UHS operates in add a further structural dimension: a new competitor cannot simply build a facility in a market where UHS holds existing CON approvals. The barriers to replicating the referral network are both relational and regulatory.

The financial expression of this pillar is in the volume consistency. Same-facility behavioral health admissions have grown in each of the past two years despite reimbursement uncertainty, and the first quarter of 2026 confirmed the trajectory with adjusted admissions up 1.2% and revenue per adjusted admission up 6.2%.

Financial Evidence

The moat is genuine on both dimensions. The structural economics of behavioral health are defensible competitive characteristics that do not depend on legislative outcomes. The referral network density, built over 47 years and expressed in consistent volume and pricing growth, compounds with time and becomes more defensible as the facility count grows. What introduces conditionality is the role of Medicaid supplemental payments in the current margin structure. The 20.5% behavioral health operating margin reflects not only competitive position but also $1.339 billion in supplemental payment net benefits that are now being reduced under federal legislation. The structural advantages are intact. The margin level may compress as the supplemental phase-down takes effect. The spread between what UHS earns and what it costs to operate may narrow. But at 15.8% ROIC in 2025, against a decade average of approximately 13.7%, there is considerably more cushion than the reported operating margin alone suggests. The structural advantages are real and should outlast the supplemental phase-down.

3. Financial Performance

Revenue grew from $9 billion in 2015 to $17.4 billion in 2025, a compound annual growth rate of 6.7%. Acute care contributed approximately 57% of 2025 revenues at a same-facility operating margin of 12.1%. Behavioral health contributed approximately 43% at a same-facility operating margin of 20.5%. Both margins are same-facility figures reflecting the established facility base only and exclude new facilities still in their ramp-up phase, corporate overhead, and provider tax assessments. The segment generating the smaller share of revenues generates the higher quality economics. The consolidated margin of 11.5% is a blended figure that simultaneously understates the behavioral health business and overstates the acute care one. The gap between the blended same-facility segment margin of approximately 15% and the consolidated margin of 11.5% is explained primarily by approximately $515 million in corporate-level operating costs not allocated to either segment, together with startup losses at recently opened facilities, most notably the $49 million pre-tax loss at Cedar Hill Regional Medical Center in its first year of operation.

The revenue trend also needs a specific adjustment. The $1.339 billion in Medicaid supplemental payment net benefits recorded in 2025 is embedded within reported revenues and operating income. That figure was approximately $1.016 billion in 2024 and around $629 million in 2023. A portion of the margin expansion over the past two years reflects the scaling of supplemental programs, not organic competitive improvement. Those programs are now in legislatively mandated decline.

Operating margins tell the decade’s story most directly. The margin was 13.75% in 2015. It compressed steadily through the late 2010s as physician costs and labor expenses rose, then collapsed to 7.49% in 2022. Three forces hit simultaneously: the nursing shortage forced reliance on expensive temporary agency staff, physician expenses in emergency medicine and anesthesiology rose sharply, and Medicaid supplemental payment timing created a revenue recognition gap. The result was the lowest operating margin in the decade-long record, 6.26 percentage points below the 2015 level.

The segment data reveals how the two-segment structure functions under pressure. Acute care same-facility operating margin collapsed from 10.6% in 2021 to 7.4% in 2022, a 320 basis point decline driven almost entirely by the labor crisis. Behavioral health same-facility operating margin declined from 19.4% to 18.1%, a 130 basis point decline over the same period. The differential between the two segments widened to 1,070 basis points at the trough. Behavioral health held at 18.1% in both 2022 and 2023 while acute care absorbed the full force of the nursing shortage and physician cost inflation. Behavioral health was the stable anchor. Acute care was the volatile component. Acute care generates 57% of revenues and receives most of the analytical attention. The segment data shows that behavioral health was the more stable business through the cycle.

Operating margins recovered to 8.23% in 2023, 10.63% in 2024, and 11.48% in 2025. The 2022 compression was driven by identifiable external forces. When those forces resolved, the margins followed.

Diluted EPS grew from $6.76 in 2015 to $23.1 in 2025, a compound annual growth rate of 13%, against revenue growth of 6.7%. Operating income grew from $1.244 billion to $1.994 billion over the same period, a CAGR of approximately 4.8%. The difference between 4.8% operating income growth and 13% EPS growth comes almost entirely from the share count. Diluted shares fell from approximately 100.7 million in 2015 to 64.5 million in 2025, a 36% reduction over the decade. That reduction was funded predominantly through operating cash flow rather than debt issuance. The share count reduction explains most of the gap. The underlying business grew earnings at roughly half the per-share rate.

Revenue per adjusted admission grew 5.4% on a same-facility basis in acute care in 2025 and 7.5% in behavioral health. In the first quarter of 2026, the figures were 6.3% and 6.2% respectively. Both segments are growing revenue per admission faster than admission volumes, confirming that pricing rather than volume is the primary revenue driver across the business.

The OBBBA reduction phases in from 2028 on a pro rata basis, reaching approximately $432 million to $480 million annually by 2032. Using the midpoint of approximately $456 million and applying the 2025 effective tax rate of 23.4%, the after-tax earnings impact is approximately $70 million per year of additional drag once the phase-down is fully active. On the current diluted share count of 64,462 thousand, that translates to approximately $1.08 per share per year, cumulating to approximately $5.41 per share by 2032. The historical operating income CAGR of 4.8% over the past decade has added more than $1.08 per share of annual earnings power, and the buyback program has consistently amplified that per-share growth by reducing the denominator. The headwind is real, quantified, and phased over seven years. It does not reverse the compounding capacity of the business. It reduces its pace during the active phase-down window.

Capital expenditure has ranged between $609 million and $1.155 billion over the decade, averaging approximately 7% of revenues. The 2025 figure of $1.015 billion is elevated relative to the mid-decade average and reflects two specific projects: the Alan B. Miller Medical Center in Palm Beach Gardens, which opened in the second quarter of 2026 with 156 beds, and the Henderson Hospital expansion in Nevada. Management guided 2026 capex of $950 million to $1.1 billion, consistent with the current investment cycle. Once these projects complete, capex should normalize toward its historical average, releasing cash for buybacks and debt service.

ROIC started at 15.8% in 2015, held in a narrow band between 13.7% and 14.8% through 2021, then collapsed to 9.3% in 2022. The collapse had two components. Operating income fell sharply as the labor crisis and physician cost inflation compressed margins, reducing the numerator. Capital expenditure continued through the downturn, growing the invested capital base and compressing the denominator simultaneously. ROIC recovered to 10.4% in 2023, 14.6% in 2024, and 15.8% in 2025, fully returning to its 2015 level. That complete cycle recovery is the most direct financial confirmation that the underlying economics survived the 2022 trough intact. UHS generates substantial economic value above its cost of capital today. That spread faces pressure as the supplemental programs phase down. The 2022 recovery demonstrated that the underlying economics hold when external pressure resolves.

Q1 2026 Update

UHS reported first quarter 2026 results on April 28, 2026. The annual analysis above is built on full year figures. Quarterly data is included here only to test whether the 2025 thesis holds at the edges.

Same-facility acute care revenues grew 8.2% with revenue per adjusted admission up 6.3%, consistent with the price-driven growth pattern established in 2025. Same-facility behavioral health revenues grew 7.3% with adjusted admissions up 1.2% and revenue per adjusted admission up 6.2%. Both volume and pricing remain positive simultaneously. Operating cash flow of $402 million compared to $360 million in Q1 2025. The quarterly results are consistent with the annual thesis and introduce no new concerns about the underlying operational performance.

4. Capital Allocation

Over the past decade, UHS deployed capital across three primary uses: capital expenditure totaling approximately $9.2 billion, share repurchases totaling approximately $6.5 billion, and dividends totaling approximately $510 million. Capex was the dominant use of cash. The buyback program was the dominant capital return mechanism. Dividends were consistent but minimal relative to cash generation.

The buyback program is the most consequential capital allocation decision UHS has made over the past decade. The diluted share count fell from approximately 100.7 million in 2015 to 64.5 million at year-end 2025, a 36% reduction over 10 years. In 2025 alone, UHS repurchased 4.65 million shares at an aggregate cost of $899.3 million, an average price of $193.38 per share. In October 2025, the board authorized a further $1.5 billion increase to the repurchase program. As of March 31, 2026, approximately $1.298 billions of authorization remained outstanding. In the first quarter of 2026, UHS repurchased 675,000 shares at approximately $189 per share for $127.3 million, continuing the program at a consistent pace even as the share price declined from its 2025 levels.

The share count reduction at UHS was funded predominantly through operating cash flow rather than debt issuance. Total debt on December 31, 2025, including senior notes, term loan, revolving credit, and capital lease obligations, was approximately $5.2 billion. The debt to OCF ratio at year-end 2025 was approximately 2.8 times, and the interest to OCF ratio was 8.4%, both reflecting a balance sheet that carries leverage but services it comfortably at current cash generation levels.

UHS has paid a dividend in every year of the past decade. The per share amount was $0.40 through the late 2010s, fell to $0.20 in 2020, and has held at $0.80 since 2021. At $51.3 million in 2025 against OCF of $1.864 billion, the dividend consumes less than 3% of operating cash flow. UHS is not a dividend growth story. The capital return vehicle of choice is the buyback program, and the flat dividend reflects that priority.

The debt structure warrants specific attention at two points. Current maturities of long-term debt on December 31, 2025, totaled $748 million, of which $700 million represents the senior notes carrying a 1.65% coupon that mature on September 1, 2026. Those notes were issued in August 2021 when market interest rates were at historic lows. UHS expects to refinance these notes at significantly higher interest rates than the original 1.65% coupon. The September 2024 debt issuance, in which UHS placed $500 million at 4.625% and $500 million at 5.050%, is the most current reference point for UHS’s borrowing cost. Refinancing $700 million at rates in that range versus the existing 1.65% coupon would add approximately $21 million to $24 million in annual interest expense. That is manageable at current OCF levels but will partially reverse the interest expense improvement achieved in 2025, when interest expense fell from $186 million to $156 million following the September 2024 debt restructuring.

The second capital structure event is the April 2026 credit agreement amendment, which added $900 million in borrowing capacity including a $400 million delayed draw term loan designated for the pending acquisition of Talkspace, Inc. The revolving credit facility was simultaneously increased by $200 million to $1.5 billion, and the tranche A term loan was increased by $300 million to $1.455 billion. The maturity date of September 26, 2029, was unchanged. If the Talkspace acquisition closes and the $400 million delayed draw term loan is drawn, total debt will increase to approximately $5.6 billion, pushing the debt to OCF ratio toward approximately 3 times at current cash generation levels. That remains within a range UHS can service comfortably, but it reduces the financial flexibility available to absorb the OBBBA revenue headwind if it materializes more severely than management currently projects.

Stock-based compensation of $95.7 million in 2025, $99.3 million in 2024, and $87.7 million in 2023 represents a real economic cost to shareholders that does not appear as a cash outflow in the operating results. At approximately 5% of operating income in 2025, SBC is not a dominant factor in the capital allocation picture but is material enough to warrant inclusion in any honest assessment of cash generation.

The consistency of the buyback program through the 2022 trough, when OCF compressed to approximately $1 billion and UHS still repurchased shares, is the clearest expression of management’s capital allocation priorities over time.

5. Competition

UHS operates in two distinct competitive environments simultaneously. In acute care it competes against the largest for-profit hospital platforms in the United States. In behavioral health it competes against a fragmented landscape of regional operators, small single-facility providers, and not-for-profit systems, with only one publicly traded pure-play peer of meaningful scale.

HCA Healthcare

HCA is the most instructive benchmark for evaluating UHS’s acute care competitive position and the clearest illustration of why scale alone does not determine investment quality Its ROIC has averaged 16.3% over the past decade, approximately 2.6 percentage points above UHS’s decade average of 13.7%, reflecting the structural advantages of market density, purchasing scale, and clinical data infrastructure that UHS’s acute care network cannot match. The business remains operationally superior, though the margin of that advantage is narrower than it appears at first glance.

The basis for different treatment rests on two factors that interact with each other in a specific way. Approximately 45% of HCA’s revenues flow from government programs whose reimbursement rates are determined by legislative and regulatory decisions rather than market negotiation. Total debt including lease obligations of approximately $48.7 billion means that any sustained reduction in government reimbursement flows directly into a highly leveraged capital structure with relatively limited capacity to absorb it. UHS carries $5.2 billion in total debt against $1.864 billion in OCF, a ratio of approximately 2.8 times. HCA carries $48.7 billion against approximately $12.6 billion in OCF, a ratio of approximately 3.85 times.

Tenet Healthcare

Tenet generates $21.3 billion in revenues across approximately 60 hospitals and a large ambulatory surgery center network. Its operating margin of 16.1% in 2025 is the highest among the three publicly traded for-profit hospital operators, reflecting a multi-year portfolio restructuring that divested underperforming hospital assets and concentrated capital in higher-margin ambulatory care. The margin improvement is real. What requires scrutiny is the 2024 net income figure of $3.2 billion, which was inflated by approximately $3.2 billion in facility sale gains recorded in the other income line. That figure is not recurring and should not anchor any assessment of normalized earnings power.

ROIC of 11.65% in 2025 is the highest in Tenet’s available record and represents genuine improvement from a decade average of approximately 7.4%, excluding a 2017 outlier driven by a specific transaction rather than operational performance. Total debt of $13.2 billion against OCF of $3.54 billion produces a debt to OCF ratio of approximately 3.7 times, materially higher than UHS’s 2.8 times. Tenet operates no behavioral health segment and competes with UHS only in acute care, where Sun Belt geographic overlap creates some direct market competition primarily around commercial payer contract negotiations rather than patient volume.

Acadia Healthcare

Both companies operate inpatient behavioral health facilities under the same payer frameworks in largely overlapping markets. The financial divergence between them is therefore a direct expression of operational quality rather than structural differences in the competitive environment.

UHS behavioral health same-facility revenues grew 7.7% in 2025 with revenue per adjusted admission up 7.5% and an operating margin of 20.5%. Acadia same-facility revenues grew 4.9% with revenue per patient day up 2.8% and an adjusted operating margin of approximately 11.9%. UHS is growing faster, pricing better, and generating 860 basis points more margin per dollar of revenue in the same market. That divergence has persisted across multiple reporting periods and is not explained by Acadia’s current legal and regulatory difficulties alone. It reflects a structural quality difference in operational execution. The ROIC divergence makes the same point in a different register. UHS generated 15.8% ROIC in 2025 against Acadia’s 10.96%. Nearly 500 basis points of return on capital separated the two businesses operating under identical payer frameworks.

Acadia’s reported results require decomposition before any financial comparison is meaningful. The company reported a pre-tax loss of $1.066 billion in 2025, which includes a $996.2 million goodwill impairment, $151 million in legal settlement costs, and $163.6 million in transaction and investigation expenses. Stripping those items, adjusted operating income was approximately $395.5 million on revenues of $3.3 billion, producing the 11.9% adjusted margin referenced above. The debt to OCF ratio of 20 times in the competition table reflects reported OCF of $131.9 million compressed by a $147.5 million Securities Litigation settlement payment. Normalized OCF excluding that payment would be approximately $279.4 million, producing a normalized ratio of approximately 9.5 times against total debt of $2.644 billion.

The operational context compounds the financial picture. The DOJ Criminal Division issued a grand jury subpoena in September 2024 investigating admissions, length of stay, and billing practices. The SEC issued a parallel subpoena covering the same subject matter. The CEO departed in January 2026, the CFO resigned in August 2025, and the COO resigned in November 2025. The professional and general liability reserve more than doubled from $87.5 million on December 31, 2024, to $181.8 million on December 31, 2025. New commercial insurance effective September 2025 excludes sexual molestation and abuse coverage. The combination of active criminal and regulatory investigations, leadership instability makes it impossible to assess the future earnings power of the business with any confidence.

Not-for-Profit Systems

The most substantive competitive pressure UHS faces in behavioral health does not come from its publicly traded peers. Not-for-profit behavioral health systems and state-operated psychiatric facilities operate in many of the same markets under materially different financial conditions. They do not pay federal or state income taxes, can issue tax-exempt bonds at lower borrowing costs, and receive government grants and philanthropic funding that UHS cannot access. These advantages matter most in psychiatrist and behavioral health clinician recruitment, where not-for-profit systems can offer mission-driven compensation structures that attract clinical talent, and in underserved markets where the economics do not justify for-profit investment but where not-for-profit operators can absorb losses through grant funding.

The competitive pressure from not-for-profit operators is real but structurally limited. They cannot match UHS’s capital deployment capacity, national geographic reach, or management infrastructure. The behavioral health market remains highly fragmented with the majority of beds operated by small regional operators, both for-profit and not-for-profit. UHS’s scale advantage over this fragmented landscape is more competitively significant than its position relative to any single not-for-profit system. The structural shortage of inpatient behavioral health beds in the United States means demand consistently exceeds available supply across most markets, reducing the intensity of direct competition for patients relative to what would exist in a balanced market.

6. Management

Marc D. Miller — Chief Executive Officer

Marc D. Miller has served as Chief Executive Officer and President since January 1, 2021. He joined UHS in 1995 and spent 26 years inside the organization before taking the top role, progressing from operational roles at individual hospitals through Vice President in 2005, Senior Vice President and co-head of the Acute Care Division in 2007, and President since May 2009. He was elected to the board in 2006. His father founded UHS and held the CEO role from inception until the day Marc Miller assumed it. UHS has never appointed an external CEO. Managing 375 inpatient facilities across 40 states, two distinct clinical businesses operating under separate reimbursement frameworks, and reimbursement relationships spanning every major government program and commercial insurer in the United States requires institutional knowledge that takes decades to build. Marc Miller spent 26 years building it. He is 55 years old and his employment agreement runs through January 1, 2029.

That background is directly relevant to the two most consequential external challenges his tenure has covered so far. The 2022 labor crisis drove premium nursing pay to $170 million in a single quarter and collapsed operating margins to 7.49%, the lowest in the decade-long record. On the Q3 2022 earnings call Miller was direct about what had happened and specific about where the pressure was already easing, with premium pay already falling from $170 million in Q2 to $81 million in Q3. On the One Big Beautiful Bill Act, Miller described the then-published impact estimates as a worst-case scenario on the Q2 2025 earnings call, pointed to active state and federal discussions around modification, and said the legislation simply cannot be left as is. The speed and completeness of the margin and ROIC recovery from the 2022 trough reflects a management team that understood the operational levers of both segments deeply enough to pull them correctly while the crisis was still unfolding.

Marc Miller’s 2025 total compensation was $16.1 million. Base salary of $1,430,769 was approximately 9% of the total. His annual cash incentive paid at $4,292,307, the maximum permitted, after adjusted net income per diluted share reached $21.74 against a maximum threshold of $21.12 and return on capital reached 12.1%, also at the ceiling. Stock awards of $9,999,904 at grant date fair value were split equally between time-based RSUs vesting over four years and performance-based RSUs tied to three-year adjusted EBITDA net of noncontrolling interests growth. The 2023 performance-based RSUs vested at 150% of target, the maximum, after the business delivered 147% of the three-year EBITDA target. Approximately 91% of his target total compensation is variable. A CEO whose pay is predominantly performance-linked across both annual and multi-year metrics has incentives pointing in the right direction.

Alan B. Miller — Executive Chairman and Founder

Alan B. Miller is 88 years old and has served as Executive Chairman since January 1, 2021, having held the Chairman and CEO role from the company’s founding in 1979. He founded UHS the day after American Medicorp, the second largest hospital management company in the United States which he had built from nothing, was taken from him in a hostile takeover. He incorporated UHS the following day and designed the share structure so it could never happen again. He served as Chairman and CEO for 42 years before passing the role to his son. His employment agreement runs through January 1, 2027.

The 346-facility behavioral health network was constructed facility by facility over four decades under a founder who recognized the structural economics of behavioral health early and built toward them consistently. The capital allocation discipline that has reduced the share count by 36% over the past decade, funded through operating cash flow rather than debt, originates with the person who built the business. It has transferred to the person now running it.

His 2025 total compensation was $8.1 million. The largest components were stock awards of $5,062,102 at grant date fair value, a base salary of $1,073,077, and a discretionary cash bonus of $1,073,077.

Ownership and Alignment

As of March 23, 2026, Alan B. Miller held 88.9% of the company’s general voting power through his combined holdings of Class A, Class B, and Class C Common Stock. The Class B shares that most investors hold represent 88.1% of the outstanding share count and 8.7% of the voting power. BlackRock holds 7.7% of Class B. First Eagle holds 8.6%. Together they own approximately 16% of the economic float and cannot influence the outcome of any shareholder vote that Alan Miller opposes.

The 47-year record is the most direct evidence of how that authority has been used. Revenues have compounded from zero to $17.4 billion. The share count has fallen 36% over the past decade funded through operating cash flow. ROIC reached 15.8% in 2025 against a decade average of approximately 13.7%. No value-destructive acquisition of scale has been made. The concentrated control has served long-term shareholders well across this history.

7. Growth Levers & Addressable Market

Organic Behavioral Health Bed Utilization

The most capital-efficient growth lever available to UHS does not require building a single new facility. Same-facility behavioral health adjusted admissions grew 1.2% in the first quarter of 2026 against revenue per adjusted admission growth of 6.2%, confirming that pricing rather than volume remains the primary revenue driver and that the admissions gap relative to underlying demand has not yet fully closed. More than 1 in 4 American adults lives with a mental illness or substance use disorder. The infrastructure available to treat them has never kept pace with that need. UHS operates approximately 24,200 available behavioral health beds across 182 US inpatient facilities. The bottleneck is clinical labor, not demand. Every additional patient day at a facility that is already built and staffed at the margin falls almost entirely to operating income. Closing the admissions gap through recruitment and retention improvement is the highest-return use of operational energy available to this business.

Behavioral Health Capacity Expansion

UHS is simultaneously expanding the physical bed base in targeted markets. The Alan B. Miller Medical Center in Palm Beach Gardens, Florida opened in the second quarter of 2026 with 156 beds. The Henderson Hospital expansion in Nevada added capacity in one of UHS’s most commercially concentrated markets. Both projects are embedded in the 2026 capital expenditure guidance of approximately $950 million to $1.1 billion. Once these projects are complete, capex should normalize toward the historical average of approximately 7% of revenues, releasing cash for buybacks and debt service.

Thousand Branches Wellness and the Outpatient Continuum

UHS operated 119 outpatient behavioral health locations as of year-end 2025, including 16 confirmed Thousand Branches Wellness sites. The Thousand Branches concept targets patients who require step-down care after inpatient discharge or ongoing outpatient treatment without requiring hospitalization. These facilities carry no licensed beds, lower facility overhead, and a payer mix weighted toward commercial rather than Medicaid. A patient discharged from a UHS inpatient facility who continues treatment at a UHS outpatient location stays within the same network. That continuity has clinical and commercial value simultaneously. The direction is right and the unit economics of outpatient behavioral care are structurally superior to inpatient on a capital intensity basis.

Acute Care Commercial Pricing

UHS’s acute care network holds meaningful pricing leverage in its core markets. In Texas and Nevada, which together contributed approximately 33% of consolidated revenues in 2025, the concentration of UHS facilities gives commercial insurers limited ability to construct a competitive health plan without including UHS hospitals. That network density translates into structural pricing power at managed care contract renewal. Same-facility acute care revenue per adjusted admission grew 4.1% in 2025 and 6.3% in the first quarter of 2026, consistently outpacing same-facility admissions volume growth of 2.4% in 2025 and 0.9% in the first quarter of 2026. The pattern is unambiguous. Price is doing more work than volume and has been for several years. Managed care and private insurers account for approximately 33% of acute care revenues, the commercially negotiated category that drives the majority of acute care profitability. Each contract renewal cycle in markets where UHS holds density is an opportunity to compound that advantage further.

Talkspace and the Virtual Behavioral Health Platform

UHS has entered into a definitive agreement to acquire Talkspace, Inc., a virtual behavioral healthcare company, with the transaction pending at the time of this report. The April 2026 credit agreement amendment designated a $400 million delayed draw term loan specifically for the Talkspace acquisition, confirming the capital commitment.

The strategic logic is clear from UHS’s existing operational picture. The inpatient behavioral health network has been capacity-constrained by clinical staffing shortages. A virtual platform that connects patients with licensed professionals without requiring physical facility infrastructure addresses that bottleneck from a different direction. Patients who cannot access a UHS inpatient bed can receive virtual care while awaiting placement or as an alternative to inpatient admission entirely. The combined platform creates a behavioral health continuum that the inpatient network alone cannot offer.

Technology and Clinical Infrastructure

UHS is deploying a new enterprise-wide electronic health record platform across its hospital network and implementing an AI-assisted nursing platform across its facilities. Both programs are multi-year investments whose financial returns will not be fully visible in the near-term reported numbers. The competitive significance is in what they build over time. A unified clinical data infrastructure across 375 inpatient facilities generates the kind of system-wide performance benchmarking and best-practice standardization that no regional competitor operating across a smaller footprint can replicate at equivalent scale. The AI-assisted nursing platform directly addresses the labor constraint that has bottlenecked behavioral health admissions growth. If it reduces the dependency on premium agency staff and improves retention among permanent clinical employees, the margin benefit compounds across the entire behavioral health segment simultaneously. These are not near-term catalysts. They are investments in the operational foundation that the next decade of growth sits on.

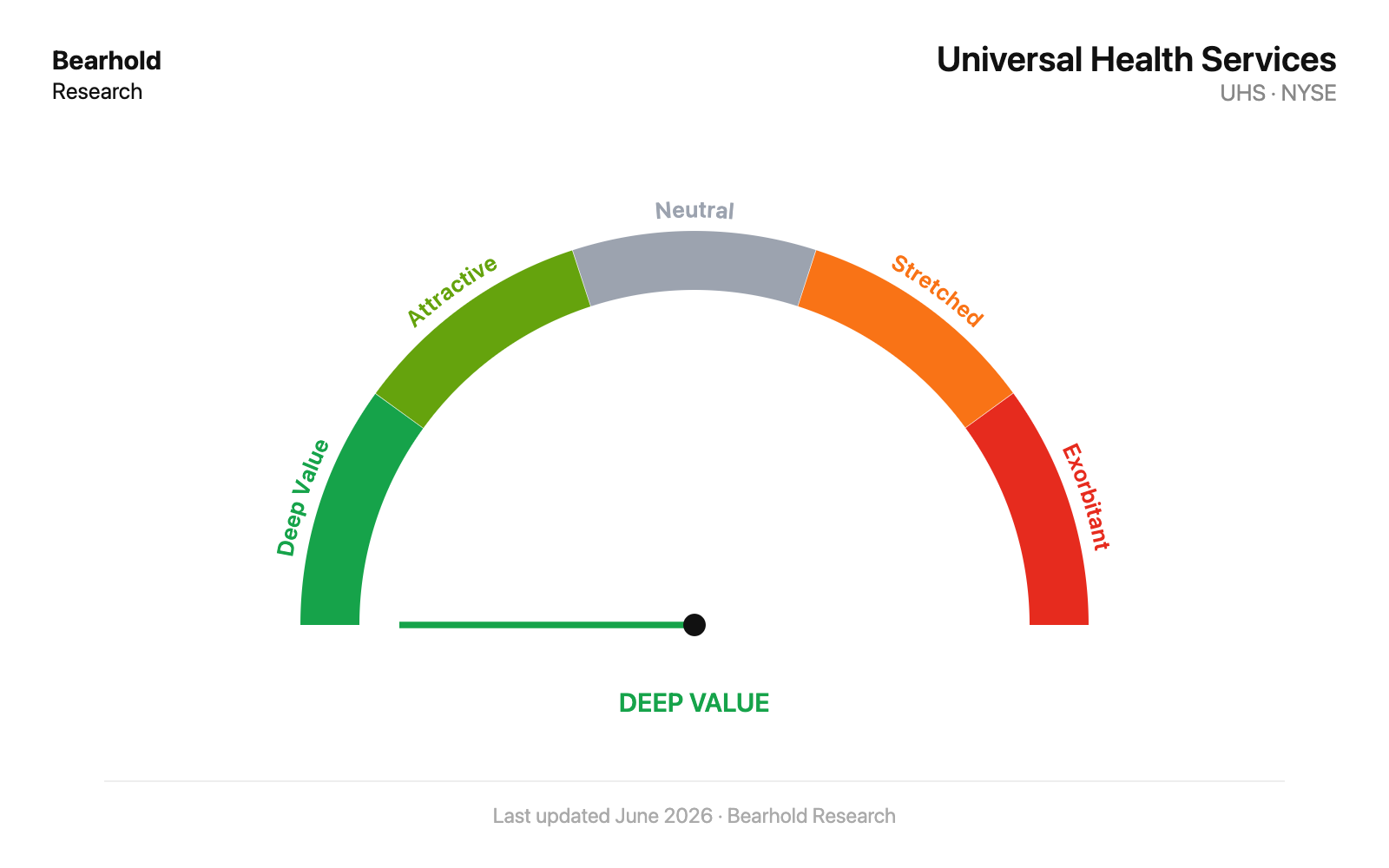

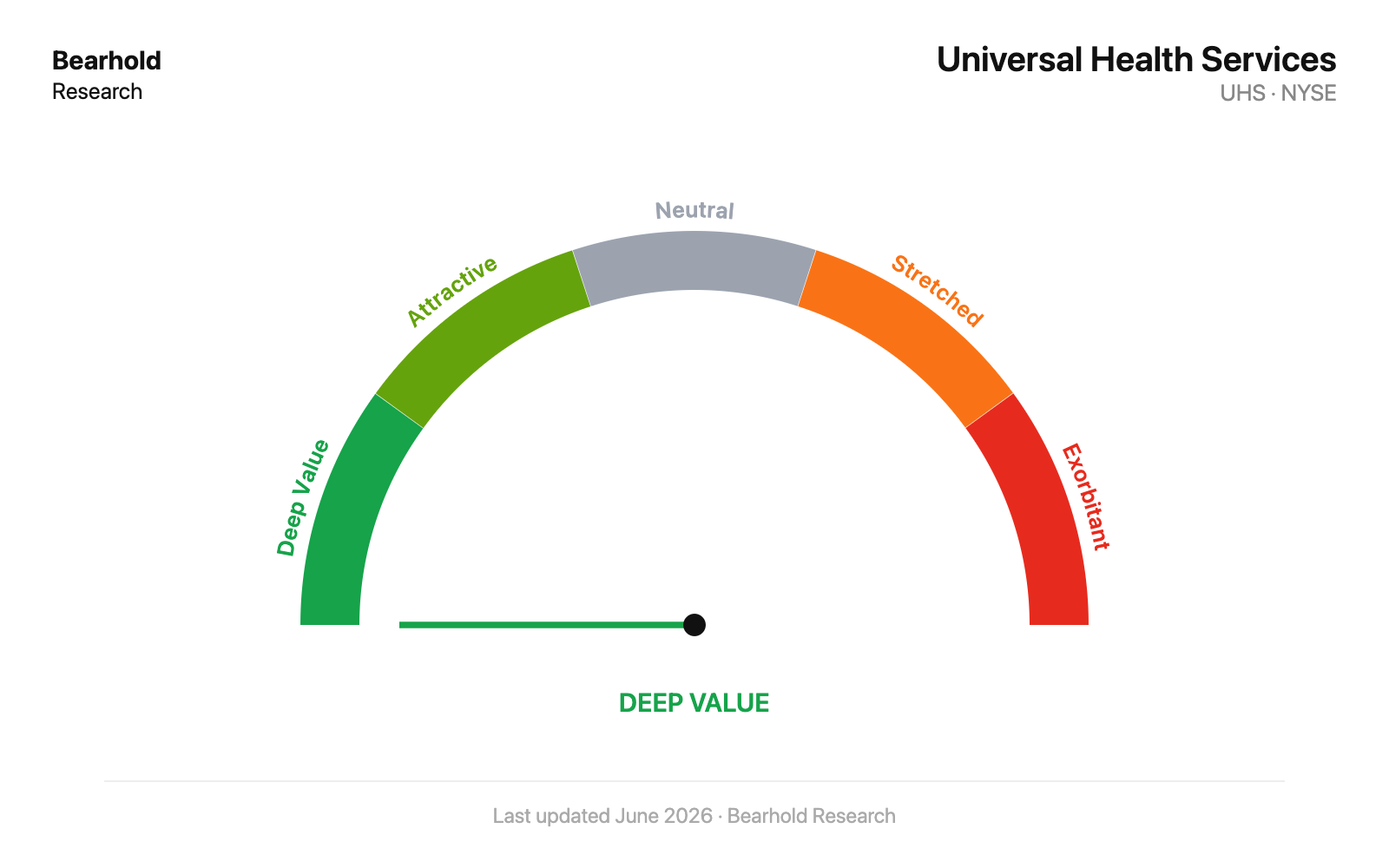

8. Valuation

The future return on UHS stock is a function of two engines: the future growth in free cash flow per share and any valuation re-rating. Both are explained below.

Free cash flow throughout this report is defined as operating cash flow less capital expenditure less stock-based compensation. SBC is deducted as a real economic cost to shareholders that does not appear as a cash outflow in the operating results.

Engine 1: Fundamentals

The first engine is the business itself. FCF per share grows over time through revenue expansion, operating leverage, and share count reduction from buybacks.

The operational component is driven by same-facility revenue growth across both segments, behavioral health at 7.7% in 2025 and acute care at 8.5%, and the improvement in FCF conversion as the current elevated capital expenditure cycle completes and capex returns toward its historical average of approximately 7% of revenues. The structural behavioral health economics, 20.5% same-facility operating margins held across a period of labor inflation and legislative headwind, continue compounding. The OBBBA phases in gradually over seven years and management has runway to offset it through volume growth and pricing discipline.

The capital return component compounds the operational growth at the per share level. UHS retired 4.65 million shares in 2025 from a diluted count of approximately 67.9 million at the start of the year. The board authorized a further $1.5 billion in repurchase capacity in October 2025 with approximately $1.298 billion remaining as of March 31, 2026. The program has run without interruption for a decade. The cash generation to sustain it is not in question at current operating levels.

Engine 2: Valuation Re-Rating

At the price of $146, the investor is paying for everything this business will earn over roughly the next 8 years, in today’s money. Everything it earns beyond that point comes to you for free. The fewer the embedded years, the more of the future the investor receives without paying for it.

UHS sits in the Deep Value zone. The expected return is the fundamental FCF per share growth rate plus a meaningful upward revaluation as the market prices in a longer earnings horizon over time. At 8 embedded years the margin of safety is substantial. The investor does not need a heroic growth assumption or a perfect regulatory outcome to generate an exceptional return. The fundamental engine delivers a strong return on its own. The re-rating is additional.

For a detailed explanation of how this valuation framework works and the thinking behind it, please check A Comprehensive Guide to Business Valuation

9. Risks

OBBBA Medicaid Supplemental Payment Reduction

The most quantified financial risk in this analysis is already legislated. The One Big Beautiful Bill Act, enacted July 4, 2025, is expected to reduce UHS’s aggregate annual Medicaid supplemental payment net benefit by approximately $432 million to $480 million by 2032, against a 2025 net benefit of $1.339 billion, representing approximately 67% of consolidated operating income that year. The reduction phases in gradually from 2028 on a pro rata basis, which gives management runway to offset through volume growth, pricing discipline, and operational improvement. The headwind operates through three simultaneous channels. The first is the direct supplemental payment reduction as the federal government caps the provider tax mechanism that funds these programs. The second is Medicaid work requirements, which may convert some Medicaid-covered patients to uninsured status, replacing government-reimbursed admissions with patients who generate little or no revenue. The third is the expiration of enhanced ACA premium tax credits at year-end 2025, which has already begun shifting exchange-insured patients to uninsured status, with exchange admissions down approximately 15% and uninsured admissions up approximately 16% in the first quarter of 2026.

The per share earnings impact of the supplemental reduction is quantified in the Financial Performance section above. Management’s possible responses shall combine political lobbying to soften the final implementation rules, admissions recovery through clinical staffing improvement, commercial pricing leverage at contract renewal, and capex normalization once the current investment cycle completes. UHS cannot meaningfully reduce its Medicaid patient volumes in response; EMTALA requires emergency treatment regardless of payer status, and behavioral health patients are structurally Medicaid-dependent in a way that makes withdrawal from the program operationally and commercially unviable. The metrics I watch most closely are same-facility behavioral health adjusted admissions growth, and revenue per adjusted admission in both segments.

Government Reimbursement Dependency

Government programs account for approximately 52% of UHS’s consolidated revenues. In behavioral health, Medicaid and managed Medicaid alone account for approximately 42% of segment revenues. The OBBBA is one manifestation of a dependency that runs deeper than any single piece of legislation. The history of Medicare and Medicaid reimbursement is a series of periodic legislative adjustments that have recurred across administrations of both parties for four decades. The scenario I monitor most closely is a slow, multi-year base rate compression where reimbursement rates are held flat or increased below the rate of cost inflation. That version of the risk affects every government payer admission simultaneously and has no discrete offset available to management.

Legal Exposure

Cumberland Hospital for Children and Adolescents is a defendant in multi-plaintiff litigation in Virginia relating to allegations of inappropriate sexual contact by a former independent contractor medical director. A September 2024 jury verdict awarded three initial plaintiffs $60 million in compensatory damages and $180 million in trebled damages under the Virginia Consumer Protection Act, with punitive damages subsequently reduced to a combined maximum of $1.05 million. UHS Inc. and UHS Delaware were dismissed as defendants during the September 2024 trial for the initial three plaintiffs, leaving Cumberland itself as the defendant. However, UHS Inc. and UHS Delaware remain named defendants for the approximately 40 additional plaintiffs still pending, with the next trial tentatively scheduled for August 2026. Aggregate insurance coverage of approximately $143 million remains under commercial policies applicable to the 2020 policy year. Commercial insurance commencing March 2025 excludes coverage for sexual molestation or abuse. Any future claims of this nature fall directly to the balance sheet with no insurance offset.

UHS Delaware is separately a primary named defendant in Washoe County, Nevada, where a September 2025 jury verdict awarded approximately $4.7 million in compensatory damages and $500 million in punitive damages. UHS Delaware intends to challenge the verdict in post-judgment proceedings and on appeal. The Cumberland insurance exclusion is the element I watch most closely. It creates an open-ended balance sheet exposure for the category of claim that has already produced the largest verdict in the company’s recent litigation history.

Dual-Class Governance

Alan B. Miller holds 88.9% of the company’s general voting power. No external shareholder action can change strategic direction, management succession, or capital allocation priorities without his agreement. Alan Miller is 88 years old. The transition of that concentrated voting authority has no publicly disclosed roadmap and no structural mechanism that gives Class B shareholders any role in shaping its outcome. The 47-year record argues in favor of the structure. What it cannot provide is a corrective mechanism if that record were ever to change. That asymmetry is permanent.

California Staffing Regulations

New acute psychiatric hospital staffing regulations in California became effective June 1, 2026, following a postponement that allowed the California Department of Public Health to assess public comments. The regulations require staffing standards specific to acute psychiatric hospitals and determination of appropriate licensed staffing based on patient acuity and care needs. California contributed approximately 11% of consolidated revenues and 13% of income from operations in 2025. The specific financial impact will depend on UHS’s ability to recruit and retain the required clinical staff at its California facilities. The scenario I monitor is whether additional states where UHS operates adopt mandatory staffing ratios at comparable levels, which would compound the aggregate annual cost impact beyond what California alone implies.

10. The Verdict

Universal Health Services is Approved in the Bearhold Universe on the strength of a behavioral health platform that has demonstrated genuine structural durability across a full decade and through a period of serious adversity.

The case rests on three things. The behavioral health structural economics. The 2022 recovery. And the balance sheet that makes it possible to hold through a period of regulatory pressure that has caused comparable operators to be treated differently.

The behavioral health platform is the foundation. The 346-facility inpatient network generates 20.5% same-facility operating margins, held across a period of labor inflation, reimbursement uncertainty, and an active federal legislative headwind. The 850-basis point differential between behavioral health and acute care margins is a structural feature of a business model built over four decades by a founder who recognized the economics of behavioral health early and built toward them consistently. The cost structure that produces those margins, labor-dominant with no surgical theaters or imaging suites, generates revenue by daily census across an average length of stay of 13.7 days. That cost structure produces margins that acute care cannot match and has done so across multiple reimbursement cycles.

The 2022 recovery is the most analytically important single data point. Premium nursing pay reached $170 million in a single quarter. Operating margins collapsed to 7.49%, the lowest in the decade-long record. Three external forces hit simultaneously. A franchise with structurally weakening competitive advantages does not recover from that combination in a single year. UHS recovered in a single year. By 2023 operating margins had already returned to 8.23%. By 2025 they had reached 11.48%. ROIC recovered from 9.3% in 2022 to 15.8% in 2025, fully returning to its 2015 level.

The risks are real and have been stated plainly. The One Big Beautiful Bill Act will reduce the aggregate annual Medicaid supplemental payment net benefit by around $432 million to $480 million by 2032. Government programs account for approximately 52% of consolidated revenues and that dependency is a permanent feature of the business model. The Cumberland litigation carries an open-ended balance sheet exposure following the commercial insurance exclusion for sexual molestation and abuse. The dual-class governance structure concentrates 88.9% of voting power in a single person with no publicly disclosed succession roadmap. None of these risks changes the Approved designation.

What distinguishes UHS from comparable hospital operators facing the same regulatory environment is the balance sheet. UHS carries total debt of approximately $5.2 billion against operating cash flow of $1.864 billion, a ratio of approximately 2.8 times. HCA Healthcare, the most operationally superior for-profit hospital platform in the United States, carries approximately $48.7 billion in total debt against approximately $12.6 billion in OCF, a ratio of approximately 3.85 times. Both businesses face structural government reimbursement dependency. The primary distinction between the two businesses is not competitive quality. It is balance sheet resilience under regulatory pressure. UHS can absorb a sustained regulatory headwind without its financial flexibility narrowing to a point that forces operational compromise. That is why one earns Approved and the other does not.

The behavioral health structural economics are genuine and durable. They hold independent of the legislative environment that determines what the government pays. The referral network density, built over 47 years, compounds with time. The balance sheet provides the durability to hold through regulatory pressure. What I watch from here is the pace of behavioral health admissions recovery and the trajectory of the supplemental payment phase-down. If the admissions gap closes as the staffing environment continues to normalize and the OBBBA impact tracks management’s base case rather than the worst case, the investment case strengthens from an already compelling starting point.

Disclosure: The author holds a position in Universal Health Services, Inc. This report reflects the author’s personal views and is not investment advice. Investing carries the risk of permanent capital loss. Read the full disclaimer here