Under The Hood - Sprouts Farmers Market, Inc.

Company Analysis & Valuation

My initial concern with Sprouts was straightforward, Walmart, Kroger, and Costco had all moved into organic, and a small-box specialty grocer built around produce would eventually get squeezed. That concern was reasonable, but it was missing something.

Sprouts is not a produce stand with a grocery section attached. It is a full grocery store built around a different philosophy, same categories as any conventional supermarket, but the sequencing, the curation, and the supply chain behind it are fundamentally different. Adding an organic aisle to a supercenter is not the same as rebuilding an entire store around fresh food. Those are two different operations, and conflating them was the flaw in my original thinking.

By the time Walmart and Kroger meaningfully expanded their organic offerings, Sprouts already had decades of site selection data, supplier relationships, and a customer base with established shopping habits. That accumulation is not something a competitor can shortcut, and the competitive pressure I was worried about had been building for most of Sprouts’ history, not arriving for the first time now.

What shifted my view was several data points together, a grocery format that is hard to replicate piecemeal, two decades of accumulated operational knowledge, margins and returns on capital that held through inflation and a store closure cycle, and a supply chain built specifically to support a freshness claim.

The author does not hold a position in Sprouts Farmers Market, Inc. at the time of publication. This report reflects the author’s personal views and is not investment advice. Investing carries the risk of permanent capital loss. Read full disclosure here.

1- The Business

Sprouts Farmers Market is a specialty grocery retailer built around fresh, natural, and organic products, operating 483 stores across 25 states as of the most recent quarter. The standard store format runs between 21,000 and 25,000 square feet, trimmed down from an older prototype of roughly 28,000 square feet.

Produce occupies the center of every store, about 20% of selling space, and anchors the shopping experience from the moment you walk in. Revenue in fiscal 2025 split 57% perishables and 43% non-perishables, a breakdown close enough to a conventional grocery basket that Sprouts carries the category breadth for a full weekly shop.

The freshness claim is backed by real infrastructure. Sprouts self-distributes nearly all of its produce through six company-operated distribution centers in Arizona, Texas, two sites in California, Colorado, and Florida, with a third-party partner covering the Mid-Atlantic. 80% of stores sit within 250 miles of one. In 2025, Sprouts extended self-distribution to meat and seafood, a transition that caused disclosed availability challenges during the changeover. By fiscal year end, four of the six distribution centers had converted, covering approximately 70% of stores, with the remainder targeted for 2026 and a projected end state of 95% coverage. For categories not self-distributed, primarily dry grocery and frozen, Sprouts relies on two external suppliers, KeHE at approximately 52% of total purchases and United Natural Foods at approximately 12%, with the remainder sourced directly from local growers.

Sprouts Brand, the company’s private label line, made up just over a quarter of revenue in fiscal 2025 following a full assortment redesign completed that year. Within the standardized store layout, a portion of the assortment rotates, vendor products and limited availability items cycling through specific shelf space, creating a discovery dynamic that keeps part of the product mix feeling different visit to visit. The store layout itself doesn’t change, only this slice of the assortment does.

The target customer is the health enthusiast and the selective shopper, someone already seeking fresh, natural, and organic products who is willing to pay for a curated experience. The first Sprouts store opened in Chandler, Arizona in July 2002. The twenty-four years since have gone toward building the things that matter, site selection knowledge across 25 states, supplier relationships negotiated and renewed many times over, and a customer base that formed its shopping habits around this format before conventional and mass-market grocers gave it serious competitive attention.

2- The Moat

This is where the analysis gets honest, and where I spent the most time.

My first instinct was that Sprouts has no real moat. There are no switching costs, a grocery shopper can walk into Whole Foods or Trader Joe’s tomorrow with zero friction. There are no network effects. The store format, while differentiated, is not patented. A well-capitalized competitor could technically lease a 23,000 square foot space, place produce bins in the center, and call it a specialty grocer. The product is available elsewhere. The customer is not locked in.

That instinct is partially right. Sprouts does not have a structural moat in the classic sense, no membership fee forcing customers through the door the way Costco does, no proprietary technology creating dependency, no regulatory barrier protecting the category. If management stops executing well, the structure alone will not save the business. I believe that is true and worth saying clearly.

But fifteen years of intensifying competition from Walmart, Kroger, Amazon-backed Whole Foods, and Trader Joe’s, and Sprouts has expanded margins, grown returns on capital, and accelerated revenue. A business with no competitive protection at all does not produce that record. Something is working, even if it doesn’t fit neatly into a textbook moat category.

What I believe is actually protecting Sprouts is four things working together, none of which constitutes a moat individually, but which collectively create a competitive position that is genuinely difficult to replicate piecemeal.

The first is the small format real estate advantage. A 23,000 square foot store fits into dense, high-traffic neighborhoods that a conventional 50,000 to 60,000 square foot supermarket physically cannot enter. That is a structural cost and location advantage, lower construction costs, cheaper lease terms, faster path to store-level profitability, and access to real estate a Kroger or Walmart simply cannot use. No backroom storage means inventory goes directly from delivery trucks to the floor, eliminating a cost layer that conventional grocers carry.

The second is private label density. Just over 25% of revenue comes from Sprouts Brand products, items customers cannot find anywhere else. That is the closest thing to a switching cost that grocery retail can produce. It is not a lock-in, but it is friction, and friction compounds over time. A customer who builds a weekly shop around several Sprouts Brand products has a reason to return that has nothing to do with produce freshness or store atmosphere.

The third is the distribution infrastructure. Six self-operated distribution centers, positioned so 80% of stores sit within 250 miles of one, took years and significant capital to build. The 2025 disruption from converting meat and seafood to self-distribution is itself evidence of how difficult that transition is, even for the incumbent that designed it. A new entrant cannot buy that footprint quickly. An existing large-format competitor already has its own distribution network optimized for a different format and would need to rebuild, not adapt.

The fourth is deliberate customer targeting. Sprouts actively cycles products out of its assortment once they become mainstream items at conventional grocers, preserving the specialty status of what remains on the shelf. That curation discipline, foraging for niche, attribute-driven products and retiring them when they go mass-market, keeps the format feeling differentiated to a customer who specifically does not want to shop where everyone else shops. Maintaining that discipline requires ongoing execution, which is precisely the vulnerability, but the discipline itself is a real competitive characteristic.

Together, these four components have produced gross margins of 38-39% in a category where conventional grocers operate at 20-25%. That is not a coincidence. It is also not permanent, it requires all four components to keep working simultaneously, which brings me to the risk I cannot dismiss.

The historical record contains one clean test of what happens when execution falters. Before 2019, under different leadership, Sprouts competed on aggressive produce promotions and loss-leader discounts, built stores averaging 30,000 square feet, and chased the price-sensitive shopper it was never going to win against Kroger or Walmart. Gross margins were stuck between 29% and 33%. The stock went nowhere for years. The structure did not save the business from a strategy that was fighting the wrong battle on the wrong terms. That period is the clearest evidence that the competitive position described above is real but not self-sustaining, it requires the right strategy to activate it.

The honest conclusion is that Sprouts has a narrow but real competitive position, not a wide structural moat. The four components working together create something durable enough to have survived fifteen years of serious competitive pressure. Whether they survive the next fifteen depends on execution remaining disciplined, which is a different and harder underwriting bet than structural protection provides.

3- Financial Performance

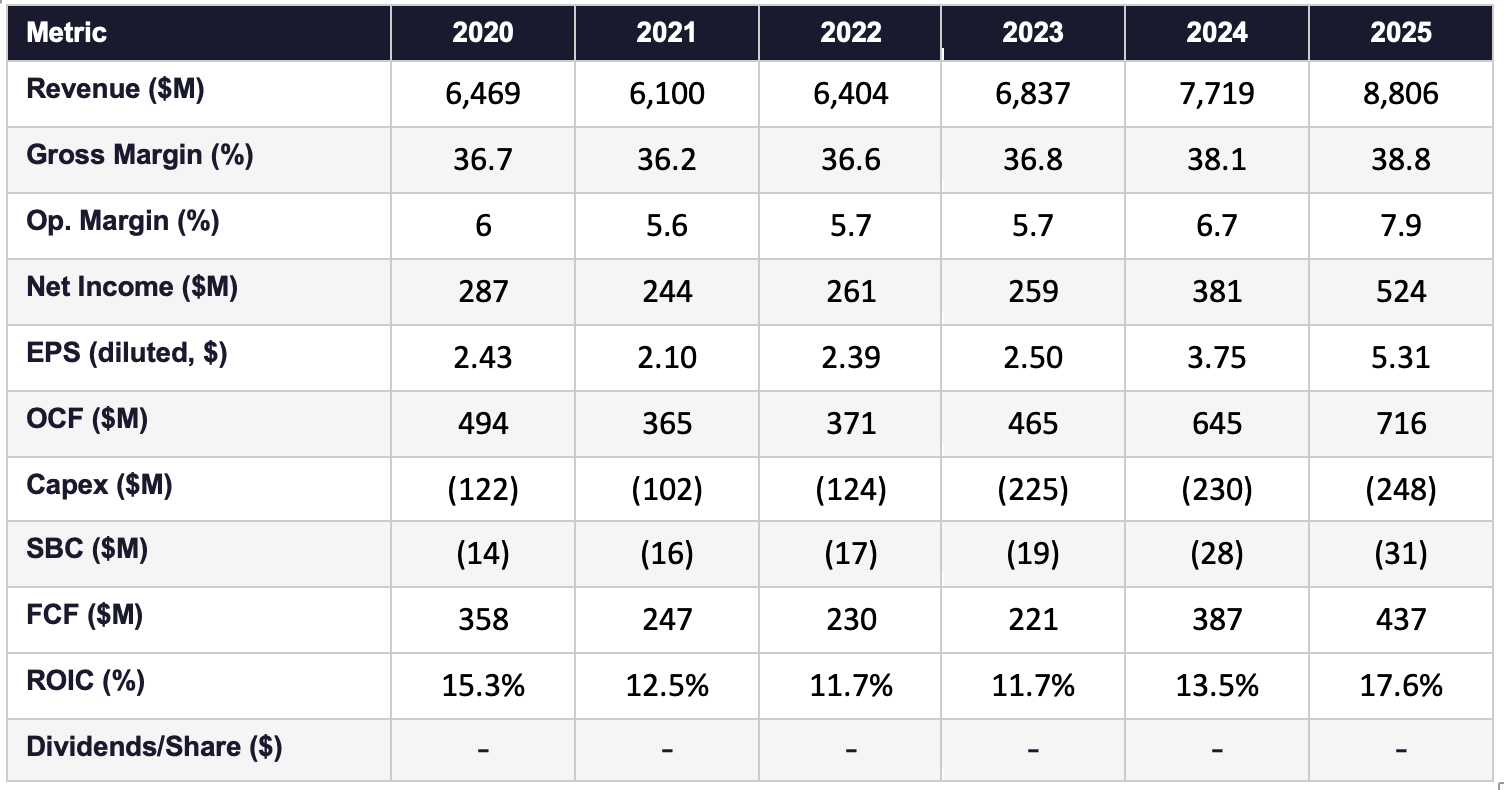

Revenue grew from $6.1 billion in 2021 to $8.8 billion in 2025, a compound annual growth rate of approximately 9.6%, accelerating to 14% in 2025 on new store contribution and a 7.3% increase in comparable store sales.

Reading that comp sales trend correctly requires understanding something specific about perishables. Produce makes up the majority of the 57% perishables revenue, so reported comparable store sales are sensitive to the price of underlying crops, not just transaction count. When produce prices spike, comps for that period can look stronger than underlying volume justifies, and the following period is then measured against an inflated base. That is precisely what the most recent data shows. Comparable store sales ran at 3.4%, 7.6%, and 7.3% for 2023 through 2025 before turning negative 1.7% in the thirteen weeks ended March 29, 2026, against an unusually strong 11.7% comparison quarter a year earlier. Stacked across both periods, two-year growth is still approximately 9.8%, consistent with the underlying trend.

The base-effect reading is not speculative. California, where Sprouts sources 40% to 70% of its produce depending on the season, experienced severe drought conditions through 2024 and into 2025 per USDA data. Elevated produce costs during that window plausibly inflated the Q1 2025 comparison base. The Q1 2026 decline is a base effect compounded by a documented weather event. This pattern has happened before, comparable store sales turned negative in 2021 as the business lapped the extraordinary grocery stockpiling of 2020, recovered cleanly, and the underlying business was unchanged. I see the current period as the same mechanism, not a different one.

Operating margin expanded from 5.6% in 2021 to 7.9% in 2025, dipping to 5.7% in 2023 when the company closed eleven underperforming stores in a single month, stores its own disclosure described as approximately 30% larger than the current prototype and financially underperforming. The recovery from that trough to 7.9% came through two mechanisms: fixed cost leverage as the newer, smaller stores ramped up, and meaningfully better inventory shrink management in 2025, which management specifically cited as a driver of gross margin expansion in that year’s earnings release. Average square footage per store declined from 27,820 in 2023 to 27,552 in 2024 to 27,237 in 2025 as the smaller prototype entered the fleet at scale.

Over the same period, sales per square foot rose from approximately $604 in 2023 to $637 in 2024 to $678 in 2025. A shrinking average footprint and rising sales per square foot in the same period is not purely an artifact of comparable store sales growth, though it is worth noting that elevated produce prices during California’s documented drought period likely inflated the revenue numerator in 2024 and 2025. The underlying productivity trend is real, but the magnitude of the per-square-foot improvement should be read with that pricing tailwind in mind.

ROIC held in a range of 11.8% to 13.6% from 2021 through 2024 before climbing to 17.6% in 2025 alongside the margin recovery. The capital-light model contributes: Sprouts leases nearly all stores and distribution centers, keeping capital expenditure low relative to revenue and funding new store growth largely from free cash flow.

Diluted EPS grew from $2.10 in 2021 to $5.31 in 2025, faster than revenue. Part of that is operating leverage and margin expansion. Part is buybacks: diluted share count fell from 116.1 million to 98.7 million over the period, a 15% reduction, funded from free cash flow rather than debt.

Sprouts carries no outstanding funded debt as of fiscal year end 2025. The credit facility exists, a $600 million revolving line maturing in 2030, but nothing is drawn against it. The largest liability on the balance sheet is lease obligations, $1.86 billion in operating leases tied to 477 store and distribution center locations with terms extending through 2048. That is not leverage in the conventional sense. It is the contractual footprint of a business that leases rather than owns its real estate, and every new store opening adds to it. The liability grows because the business is expanding, not because it is borrowing to survive.

One of the cleaner financial decisions under the current leadership was eliminating the funded debt entirely, $125 million repaid in each of 2023 and 2024, while simultaneously running a buyback program funded from the $716 million in operating cash flow the business generated in 2025 alone. The balance sheet today reflects a business that finances its growth from operations, not from the credit markets.

Sprouts has not paid a dividend since its 2013 IPO and does not plan to. The entire return to shareholders runs through buybacks, $203 million in 2023, $228 million in 2024, and $472 million in 2025, all from free cash flow. Diluted shares fell from 116.1 million in 2021 to 98.7 million in 2025. Each remaining share carries a growing claim on a growing pool of earnings. There is no dividend check, the return runs through a shrinking denominator against a growing numerator.

4- Management

Jack Sinclair has served as Chief Executive Officer since June 2019. Before joining Sprouts, he spent more than three decades in grocery retail, fourteen years at Safeway in the United Kingdom, followed by eight years as Executive Vice President of Walmart’s entire U.S. grocery division, responsible for operations across more than 4,000 stores. He served briefly as CEO of 99 Cents Only Stores before joining Sprouts.

What Sinclair actually changed at Sprouts is worth being precise about, because the temptation is to attribute everything that improved after 2019 to his arrival. Revenue growth was already happening before he arrived, the format and the category tailwind were working regardless of who was running the company. What Sinclair specifically changed was the margin structure. He stopped the aggressive loss-leader promotions. He engineered the smaller store prototype. He pushed private label penetration from a modest base to over 25% of revenue. He initiated the self-distribution buildout for meat and seafood. Gross margin went from 33-34% under prior leadership to 38.8% by 2025. That is his contribution, not the top line, the bottom line.

The succession question matters here because Sinclair is 64, and the margin structure he built is the primary thing an investor in this business is underwriting. I thought carefully about whether the performance of the last six years is person-dependent in a way that creates a real holding risk.

My conclusion is that it is less person-dependent than it initially appears, for a specific reason. Sprouts has had multiple CEO transitions since 2002 and revenue growth continued through all of them, including through the leadership vacuum between Amin Maredia’s departure in December 2018 and Sinclair’s appointment in June 2019. That is a pattern of a format with enough operational momentum to carry through leadership gaps. What changes with leadership is the strategic direction, and the risk is not a leadership transition per se but a strategy drift that takes the business back toward competing on price against Walmart and Kroger.

The bench Sinclair has assembled is the specific reason I think that risk is manageable. Nick Konat, President and Chief Operating Officer, joined in March 2022 from Petco where he was Chief Merchandising Officer, and before that spent nearly a decade at Target running food operations and private label development. He is the person actually running day-to-day store operations, supply chain, and product innovation, the current strategy is his execution as much as Sinclair’s design. Don Clark, appointed Chief Merchandising Officer in February 2026, brings deep specialty retail sourcing experience. Amanda Rassi, appointed Chief Customer Officer at the same time, oversees the loyalty program and digital data strategy. Curtis Valentine as CFO is the capital allocation gatekeeper who has been the architect of the buyback program and the self-distribution investment decision.

The risk of strategy drift after a CEO transition is real. But a board that replaced Sinclair with someone who decided to abandon small-format stores, drop private label, and compete on bulk produce discounts would be dismantling the margin structure it spent six years building.

Insider ownership is small, all directors and executive officers as a group held approximately 1.3% of shares outstanding as of March 2026, with Sinclair individually below 1%. The largest shareholders are institutional, Vanguard at 11.3%, Fidelity at 10.5%, and BlackRock at 9.9%. This is not a founder-controlled company, which is a real governance consideration for an execution-dependent business.

5- Competition

Sprouts operates in a large, fragmented, and highly competitive industry with few barriers to entry, per its own filings. The directly comparable specialty formats are Whole Foods Market, Trader Joe’s, and Natural Grocers by Vitamin Cottage.

Whole Foods has operated as an Amazon subsidiary since 2017 and reports no separate financials. It competes on broader assortment and national brand equity built over three decades, with Amazon’s logistics network and Prime membership integration behind it. Its stores run larger than the Sprouts prototype, which cuts the other way on cost structure and shopping trip efficiency.

Trader Joe’s is privately held and discloses nothing. Its format is closest to Sprouts in physical footprint, small box, curated, largely private label, but the value proposition differs. Trader Joe’s competes primarily on price with higher private label penetration than Sprouts’ disclosed 25%, and a cultural brand identity that creates loyalty beyond what a rewards program delivers.

Natural Grocers is the only publicly traded name in this set. It generated $1.33 billion in net sales for the fiscal year ended September 30, 2025, roughly one sixth of Sprouts’ scale, with an operating margin of approximately 4.7% against Sprouts’ 7.9%. It is a controlled family business with a store count of 169, growing at a pace Sprouts exceeded years ago.

The mass market question, Walmart, Kroger, Costco, deserves direct treatment because it was the starting point of my concern. These retailers collectively hold the majority of U.S. organic dollar sales, and that share has grown from 46% in 2005 to 56% in 2020. That is a real fact about the category. It is not the same as being a relevant competitor for Sprouts’ specific customer.

The majority-share figure blends every organic purchase made in the country, including the price-sensitive shopper who picks up organic milk alongside laundry detergent and was never going to make a dedicated specialty grocery trip. None of these retailers has built a format around the produce-centered, curated, discovery-oriented experience Sprouts sells. Kroger folds organic into existing mainstream aisles through its Simple Truth private label. Costco competes on bulk volume and membership economics. Walmart carries organic as one line among tens of thousands of SKUs rather than as the organizing principle of the store. Their scale is a real fact about the category. It is not evidence that they are competing for the same trip.

6- Growth

Sprouts’ growth rests on two mechanisms: more stores in places it barely operates today, and more productivity from stores it already has.

The unit growth runway is real and geographically specific. California alone accounts for 156 of 477 stores, roughly a third of the entire fleet. Fourteen of the twenty-four states Sprouts operates in have single-digit store counts. Roughly half the country has no Sprouts at all. Management has stated a long-term ambition of reaching 1,400 stores nationwide. The constraint is not demand, it is distribution center density. A produce-centered format cannot operate profitably without a hub close enough to maintain freshness, which is why the self-distribution buildout is a growth enabler, not just an efficiency measure. Each new distribution center unlocks a new radius of viable store locations. Sprouts entered New York for the first time in early 2026 and has named Chicago, Boston, and the broader Midwest and Northeast as the next expansion targets once distribution capacity supports them. The near-term pipeline is more concrete than the long-term ambition: over 140 approved locations as of early 2026, against the 40-plus openings guided for 2026, a pace of approximately 10% annual unit growth.

On the existing-store side, Sprouts Rewards, launched nationally in 2025, is the data and personalization lever management is counting on to increase visit frequency and basket size through targeted offers rather than blanket discounting. E-commerce grew 10% year over year in Q1 2026 and now represents approximately 16% of quarterly sales, delivered through Instacart, DoorDash, and Uber Eats across every market Sprouts operates.

7- Valuation

At today’s price, an investor is paying for everything this business will earn over roughly the next 15 years, in today’s money. Everything beyond that comes for free.

To put that number in context, Costco and Walmart, two of the most competitively protected businesses in retail, are currently priced at above 40 embedded years. The market is paying for more than four decades of future cash flows, in today’s money, for businesses whose structural moats justify a high degree of confidence in that long-term earnings stream. That premium is earned. Both businesses have structural lock-in mechanisms, Costco’s membership model, Walmart’s unmatched cost scale, that give an investor legitimate confidence holding through decades of uncertainty.

Sprouts at 15 embedded years is priced at less than half that level. The gap reflects two things: a smaller business with a narrower competitive position that the market is not yet willing to pay a structural premium for. Both of those are fair assessments.

What the gap also reflects is that the market has already shown what it is willing to pay for Sprouts when sentiment is favorable. When the stock peaked at approximately $180 in 2025, the implied embedded years reached 35, approaching the premium territory reserved for structurally protected businesses. That valuation was not sustainable at Sprouts’ current stage of development, and the subsequent decline to today’s price reflects both the comp sales normalization and a rational repricing of execution-dependent growth. But it is a meaningful data point. It tells us the market is capable of pricing this business at near-structural-premium levels when the financial momentum is visible, and that an investor entering at 15 embedded years today is buying at less than half of what that same market was willing to pay less than a year ago.

The return from this entry point comes from two engines. The first is the business itself, free cash flow per share growing through revenue expansion, operating leverage, and share count reduction from buybacks. The second is valuation re-rating as the market moves the price back toward a fair recognition of the business’s durability. At 15 embedded years, there is room for both engines to contribute.

Sell discipline triggers when the embedded years reach a level inconsistent with the quality and structural characteristics of the business.

8- Risks

Weather and Crop Cost Volatility

Sprouts sources 40% to 70% of its produce from California depending on the season, and produce alone accounts for approximately 20% of selling space and sits at the center of the format’s entire value proposition. That concentration is not incidental, California’s climate is uniquely suited for the variety and volume of specialty crops Sprouts’ assortment requires, and no comparable domestic alternative exists at the same scale. It is also a structural exposure that cannot be diversified away without fundamentally changing what the business is.

California experienced severe drought conditions from 2020 through 2022, with 2020 to 2022 representing the driest three-year period on record according to USDA data, followed by continued drought stress through 2024 and into 2025. The financial record through that period shows gross margin holding, Sprouts passed elevated produce costs through to customers and margins expanded rather than contracted. That is the best available evidence of pricing resilience under cost pressure, and it is a genuinely reassuring data point.

But it needs to be read carefully. The ability to pass costs through depends on competitive market conditions at the time, not on a structural pricing advantage Sprouts holds regardless of circumstances. During the recent drought period, elevated costs were an industry-wide phenomenon affecting conventional grocers and specialty retailers alike, a competitor could not undercut Sprouts on produce without absorbing the same cost pressure. That is a different situation from a Sprouts-specific cost shock in a period when competitors face no equivalent pressure, which is the scenario the record has not yet tested.

A more severe or prolonged supply disruption, a multi-year drought deeper than what California experienced from 2020 to 2022, a disease event affecting specialty crop yields, or a logistics disruption concentrated in the California growing regions, would pressure gross margin in a way the current track record does not fully address. Sprouts’ format depends on fresh produce being available, abundant, and reasonably priced relative to what the health enthusiast customer is willing to pay. If any of those three conditions breaks down for an extended period, the format’s central value proposition is impaired in a way that operational discipline alone cannot fix.

The self-distribution buildout partially mitigates this by improving freshness and reducing spoilage in transit, which protects margin from the shrink side rather than the cost side. But it does not change the sourcing geography or the fundamental California dependency. This is a risk that warrants monitoring at every earnings cycle.

Execution Dependency

This is the risk I think about most with Sprouts, and the one that most distinguishes it from the other names in the Bearhold universe.

The competitive position described in the moat section requires four components working simultaneously, small format real estate, private label density, tight distribution infrastructure, and deliberate customer targeting through continuous product curation. None of those four protects the business on its own. But the mechanism that connects them is strategy, not structure. If the strategy changes, the margins change. There is no membership fee forcing customers through the door, no network effect deepening with scale, no switching cost keeping the health enthusiast from walking into Whole Foods or Trader Joe’s tomorrow. The business earns its competitive position every day through execution, and it has to keep earning it.

The pre-2019 period is the clearest empirical evidence of what happens when execution is average. Under prior leadership, Sprouts competed on aggressive loss-leader produce promotions and discount couponing, built stores averaging 30,000 square feet, and chased the price-sensitive shopper it was never going to win against Kroger or Walmart on their own terms. The result was gross margins stuck between 29% and 33%, a stock that went nowhere for years, and a business that looked structurally similar to what Sprouts is today, same format, same category, same distribution infrastructure, but produced a fundamentally different financial outcome because the strategy was wrong. The structure did not save it. The right strategy, executed consistently, is what produced the improvement. That is the lesson and the risk at the same time.

The specific form execution dependency takes at Sprouts is strategy drift, the risk that a future leadership change, a board that loses patience during a period of weak comps, or an activist pushing for mass-market expansion causes the business to abandon what works in pursuit of a broader customer that will never be loyal to a specialty format on price terms. That scenario does not require management to be incompetent. It requires one strategic decision to go the wrong way, and the financial consequence would be visible in margins within few quarters. The bench Sinclair has assembled, Konat, Clark, Rassi, Valentine, are the people who built and optimized the current playbook, which mitigates but does not eliminate this risk. A board can always make a different decision, and at 1.3% insider ownership there is no controlling shareholder to prevent it.

Mass Market Channel Share

Conventional supermarkets, club stores, and supercenters have held the majority of U.S. organic dollar sales since the mid-2000s, and that share has grown, from 46% in 2005 to 56% in 2020 according to USDA data citing the Organic Trade Association. That trajectory did not slow Sprouts’ margin expansion or revenue growth over the same period, which is the most important context for reading this risk correctly. The mass market gaining share of organic spending and Sprouts expanding margins simultaneously are not contradictory, they reflect two different customers making two different decisions.

The mass market organic buyer is the price-sensitive, opportunistic shopper who picks up organic milk or bananas as one line inside a much larger conventional basket. That customer was never Sprouts’ customer, and Kroger gaining more of their spending does not reduce Sprouts’ addressable market in any direct sense. The health enthusiast who makes a dedicated trip to a specialty grocer for curated, attribute-driven products is a different person making a different decision, and the organic category’s overall growth means more of both types of buyers exist over time, not fewer.

The risk this creates for Sprouts is more subtle than the headline share number suggests. It is not that Walmart is taking Sprouts’ existing customers, the evidence does not support that. It is that as organic becomes more mainstream and more available everywhere, the category loses some of the scarcity and discovery value that makes a dedicated specialty trip feel worth making. A health enthusiast who can find a reasonable selection of organic produce, keto snacks, and gluten-free packaged goods at their regular Kroger may make fewer dedicated Sprouts trips over time, because the incremental value of the specialty trip declines as the gap in availability narrows. That is a slow-moving structural pressure rather than a acute competitive threat, and it is the version of the mass market risk worth watching. Sprouts’ response, cycling out products once they go mainstream, continuously foraging for new niche items, deepening private label penetration, is the correct strategic answer to exactly this pressure.

The Verdict

I am approving Sprouts Farmers Market.

I did not arrive at this easily. I came in worried about mass market competition and left still believing the moat is narrow. I spent time genuinely uncertain about whether the post-2019 improvement was person-dependent in a way that created a holding risk I couldn’t accept. I considered whether the negative comp sales in Q1 2026 was the first visible crack in a thesis that looked better on paper than in reality.

None of those concerns resolved cleanly. What changed my mind was the weight of evidence across the whole picture.

Fifteen years of intensifying organic competition from better-resourced competitors has not compressed Sprouts’ margins, it has watched them expand. Multiple CEO transitions have not broken revenue momentum, the format carried through all of them. The comp sales decline has a credible, historically precedented explanation tied to a documented weather event inflating the prior year base, not to a collapse in demand or traffic.

What I believe is protecting this business is not one thing but four things working together, small format real estate, private label density, tight distribution infrastructure, and deliberate customer targeting, none of which individually constitutes a classic moat, but which collectively have produced gross margins of 38-39% in a category where conventional grocers operate at 20-25%. That is the fact I keep coming back to. Margins at that level, sustained through an inflationary period and a leadership transition, do not happen in a business with no competitive protection.

The execution dependency is real and I am not dismissing it. This is not a Costco or a Walmart businesses where the structural protection is clear enough that I can hold through almost anything. With Sprouts, I am underwriting a team and a strategy in addition to a business, and that requires active monitoring. I am comfortable with that, because the team Sinclair assembled, Konat, Clark, Rassi, Valentine, are the people who built and optimized the current playbook. A succession from Sinclair to Konat would represent continuity.

The author does not hold a position in Sprouts Farmers Market, Inc. at the time of publication. This report reflects the author’s personal views and is not investment advice. Investing carries the risk of permanent capital loss. Read full disclosure here.