Under The Hood, ResMed ($RMD)

Company Analysis and Valuation

The Outlook

There is a condition that affects nearly one billion people on earth. Most of them don’t know they have it. Their doctors haven’t diagnosed it. Their partners have complained about the snoring, the gasping, the restless sleep, but the link to a treatable medical condition has never been made. Obstructive sleep apnea, or OSA, is one of the most prevalent and undertreated chronic conditions in modern medicine, and ResMed has spent thirty years quietly building the most comprehensive platform for diagnosing, treating, and managing it.

This is not a story about a niche medical device company. It is a story about a platform business with thirty million cloud-connected patients, a proprietary data advantage that compounds with every device sold, and a software layer that makes it operationally difficult for the healthcare providers who use it to switch to anyone else. The hardware is just the door into the ecosystem.

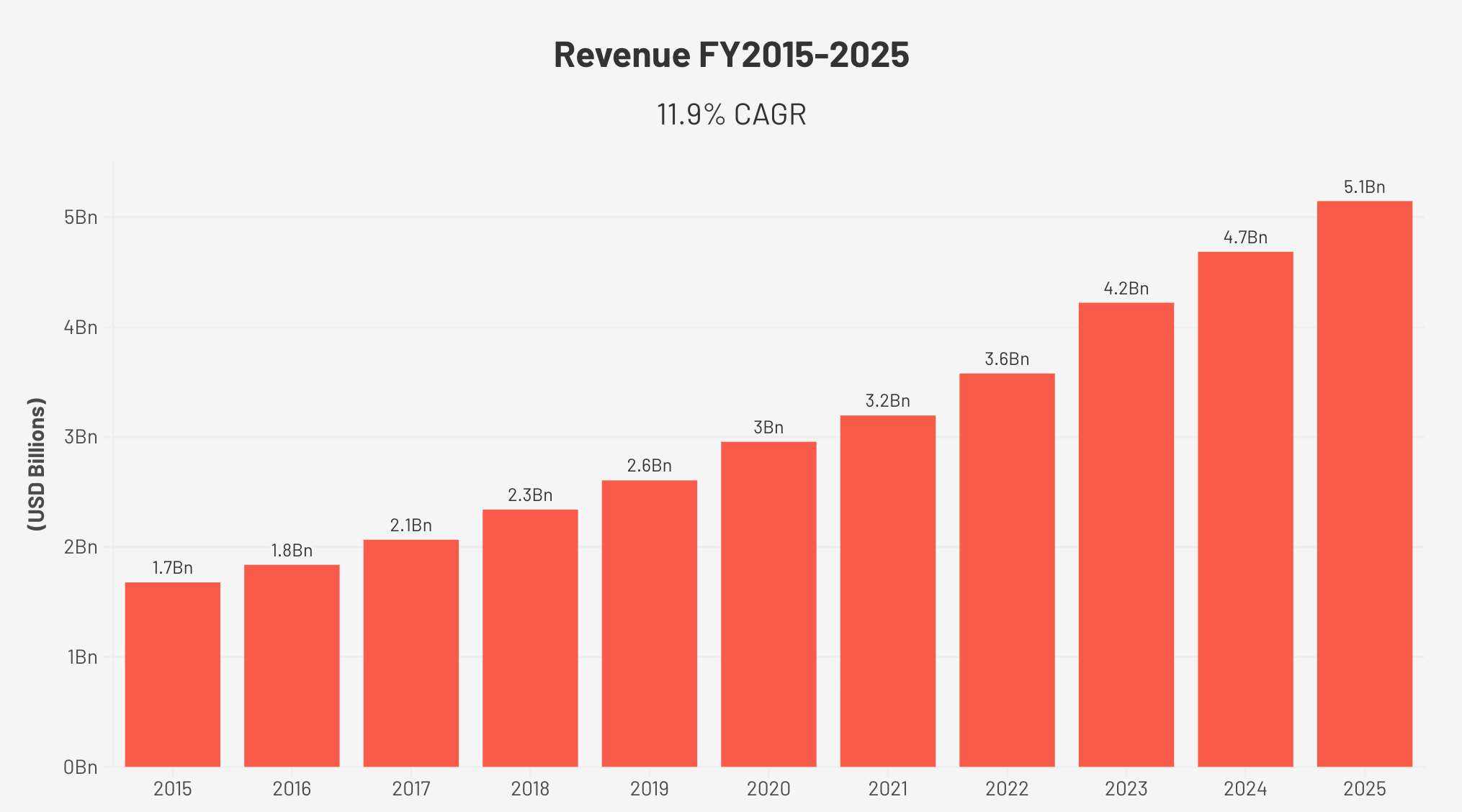

Revenue has grown at 11.9% annually for a decade. Operating margins have expanded from 24% to 33%. Free cash flow has increased more than fivefold. And yet fewer than 20% of the people who need this product have ever received it.

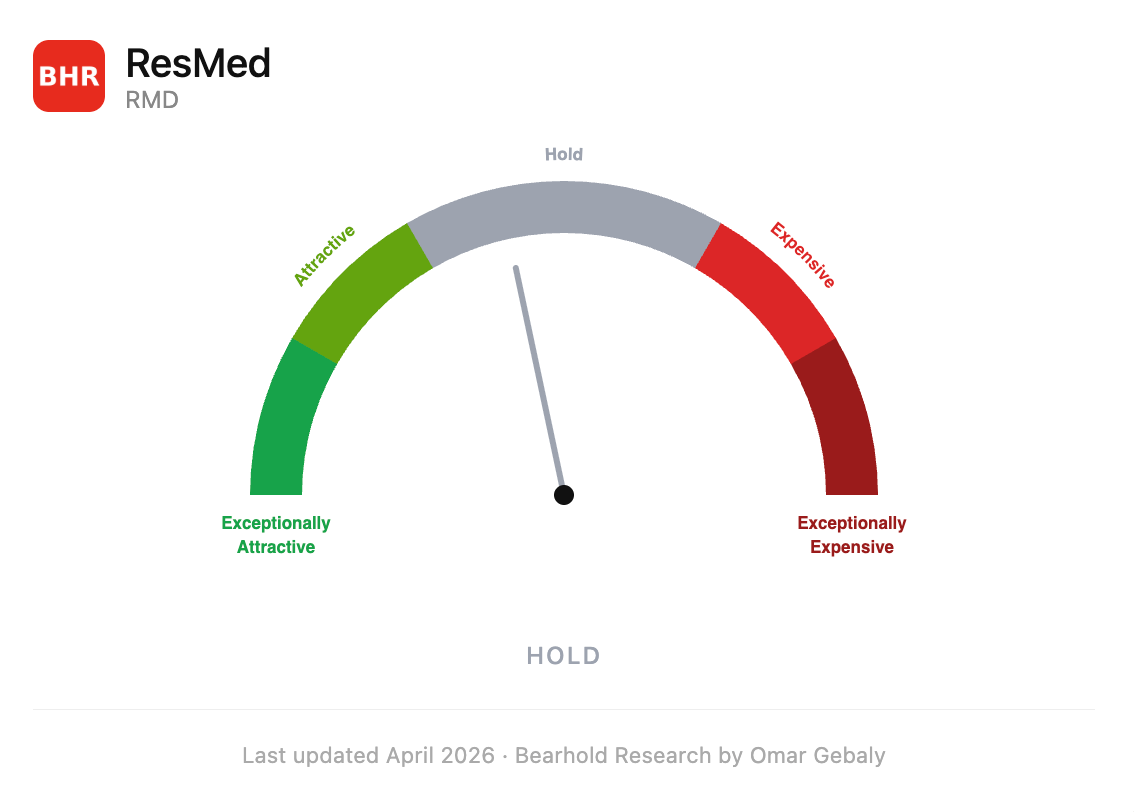

The stock is not cheap. At 23 years of embedded cash flows, ResMed sits in the Hold zone of the Bearhold valuation framework, a fair price for a business of exceptional quality. I am not buying here. But I am watching, and this report explains exactly what I am waiting for.

At a Glance

Company: ResMed Inc.

Ticker: $RMD · NYSE

Sector: Healthcare

Industry: Medical Devices & Instruments

Market Cap: $32.65 billion (at $224)

Dividend Yield: ~0.95% ($2.12 per share, FY2025)

Status: Approved, Bearhold Universe

First Coverage: April 2026

Valuation Zone: Hold (last updated April 2026)

Disclaimer: This report reflects the author’s personal views and is not an investment advice. Investing carries the risk of permanent capital loss. Read the full disclaimer here

The author does not currently hold a position in $RMD at the time of publication.

1. The Business

What the Company Does

ResMed makes the devices and software that treat sleep-disordered breathing. The flagship products are CPAP (Continuous Positive Airway Pressure) and APAP (Automatic Positive Airway Pressure) machines, compact bedside devices that deliver pressurised air through a mask while the patient sleeps, keeping the airway open and eliminating the breathing disruptions that cause OSA. The condition, if left untreated, is associated with hypertension, stroke, type 2 diabetes, and coronary artery disease, which is why the clinical community increasingly treats it as a cardiovascular risk factor, not just a sleep nuisance.

Revenue breaks down into three streams: devices at approximately 52% of the total, masks and accessories at 36%, and Residential Care Software at 12%. The structure matters. Devices are event-driven, a patient buys one at diagnosis and replaces it every few years. Masks are recurring, replaced every three to six months for as long as the patient stays on therapy. Software is subscription-based. The combination produces a revenue profile far more stable than a pure device company, with the recurring mask and software streams anchoring the base even in softer device years.

How the Business Was Built

ResMed traces its origins to June 1989, when Dr. Peter Farrell founded the company, originally called ResCare, in Sydney, Australia, to commercialise nasal CPAP technology invented by Professor Colin Sullivan at the University of Sydney in 1981. Baxter Healthcare had licensed the technology and then decided not to pursue it. Farrell recognised what Baxter had missed.

ResMed Inc. was incorporated in Delaware in March 1994 and went public on June 1, 1995, trading on NASDAQ. The company moved its primary listing to the New York Stock Exchange in September 1999.

For its first two decades, ResMed was a device company that grew by making better CPAP machines and expanding geographically. The inflection came around 2014, when the company began embedding cellular connectivity into devices as standard, a decision that looks obvious in hindsight but required genuine conviction at the time. Connected devices enabled remote monitoring at scale. Clinicians could adjust therapy settings without requiring patients to return to a clinic. And every connected patient became a source of real-world clinical data. That data now feeds the machine learning algorithms that make each new device generation smarter than the last. Today, ResMed manages over 30 million cloud-connected patients through its AirView platform, with more than 10 million active on myAir, the patient-facing therapy management app.

The flywheel is real: more patients generate more data, which improves therapy outcomes, which attracts more patients and more providers into the ecosystem.

The Philips Recall, and What Actually Happened

In June 2021, Philips issued a recall of millions of CPAP, bilevel, and ventilator devices after discovering that the polyester-based sound abatement foam inside the machines was degrading and potentially releasing particles and gases into the patient’s airway. It was a significant product safety failure that triggered multi-billion euro legal settlements and years of operational disruption for Philips.

ResMed was the only large-scale alternative with the manufacturing capacity to absorb displaced patients quickly. The impact on ResMed’s numbers was real but more targeted than widely reported. Overall revenue growth remained broadly consistent with historical trends. The visible surge was concentrated in the US, Canada, and Latin America device segment specifically, where device revenue grew approximately 24% in FY2022 and approximately 35% in FY2023, compared with around 9% in the year before the recall. By FY2024, device growth in that segment had normalised to approximately 11%, and FY2025 came in at 9.8% for total revenue, a return to the underlying demand trajectory. The recall pulled forward some volume and concentrated it geographically, but the business was not propped up by it.

Scale

ResMed employs more than 10,600 people across more than 140 countries. The US, Canada, and Latin America generate approximately 58% of Sleep and Breathing Health revenue. Combined Europe, Asia, and other markets contribute approximately 29%. Residential Care Software, sold only in the US and Germany, rounds out the remaining 12%. Manufacturing is split across Australia, Singapore, and the US, with the company running an active foreign currency hedging programme to manage the exposure this creates.

2. The Moat

Four Walls, One Ecosystem

ResMed’s competitive position is not a single advantage, it is four advantages that reinforce each other.

The first is clinical data. ResMed has more real-world sleep therapy data than any organisation on earth. Thirty million cloud-connected patients generate continuous information, therapy compliance, apnea-hypopnea index, mask leak, breathing patterns. This data feeds the algorithms that make the AirSense 11, and whatever comes after it, progressively more effective. A competitor launching a CPAP device today faces not just a product quality gap but a data gap that will take years to close.

The second is the installed base and the recurring revenue attached to it. Thirty million active patients buying masks every three to six months is a durable annuity that does not depend on the next product launch. Patients who have established a functioning therapy routine are unlikely to switch ecosystems.

The third is the software layer. Brightree, the leading home medical equipment (HME) software platform in the US, and MEDIFOX DAN in Germany are deeply integrated into the administrative and clinical workflows of thousands of care providers. These platforms are not standalone software businesses, they are the connective tissue between device sales and the care delivery system. When a provider uses Brightree to manage billing, patient records, and inventory, switching to a competitor means disrupting those workflows entirely. That is a meaningful switching cost that goes well beyond product preference.

The fourth is regulatory and clinical credibility. ResMed’s devices are approved across virtually every major regulatory jurisdiction globally, supported by decades of peer-reviewed clinical evidence. New entrants face not just a commercial challenge but a multi-year regulatory validation process. That is a barrier that does not exist in consumer device categories.

The Wearables Tailwind

An often overlooked accelerant is the integration of OSA detection into consumer wearables. Apple Watch and Samsung Galaxy Watch now feature FDA (US Food and Drug Administration)-cleared breathing disturbance detection. These devices are identifying undiagnosed OSA patients at population scale and nudging them toward clinical care. ResMed has positioned itself as the natural destination for that flow, its myAir app integrates directly with Apple Health and Samsung Health, and CEO Mick Farrell has explicitly described the consumer wearables ecosystem as building the company’s “data lake.” The most powerful referral engine ResMed could imagine is a device worn by hundreds of millions of people, many of whom don’t yet know they need a CPAP machine.

The Numbers Don’t Lie

The financial record is the most reliable evidence of a moat. ResMed’s operating margin expanded from 24.4% in FY2015 to 32.8% in FY2025. ROIC (Return on Invested Capital) averaged 18.9% over the decade, well above the estimated cost of capital throughout. A business losing competitive position does not do that while tripling its revenue.

The comparison with Philips makes the point most cleanly. Before the recall, Philips operated at approximately 8% operating margin in its health technology division, a level ResMed was already far above and moving away from. After the recall, Philips fell into losses in 2022 and 2023. By 2025, it had only recovered back to that same 8% baseline. Over the same period, ResMed’s operating margin continued to expand. Two companies nominally competing in the same market, on very different structural trajectories.

3. Financial Performance

A Decade in Numbers

Revenue grew from $1.68 billion in FY2015 to $5.15 billion in FY2025, an 11.9% compound annual growth rate (CAGR) over ten years. That growth was primarily organic. Two meaningful acquisitions, the Brightree HME software business in FY2016 and MEDIFOX DAN in FY2023, added inorganic revenue, but the underlying Sleep and Breathing Health segment has compounded consistently without acquisition support.

Operating margin expanded from 24.4% to 32.8%, with a ten-year average of 26.5%. Gross margin averaged 57.6% across the decade, reflecting the premium positioning of ResMed’s clinical products relative to commodity device alternatives. Net margin in FY2025 reached 27.2%, up from 21.0% in FY2015, aided in part by a below-trend effective tax rate of 16.5% due to one-time items, a level that should not be assumed to repeat.

Diluted EPS (Earnings Per Share) grew from $2.47 in FY2015 to $9.51 in FY2025, a 14.4% CAGR. The share count has been essentially stable over this period, rising only 3.2% from 142.7 million to 147.3 million diluted shares. EPS growth here reflects genuine business improvement rather than financial engineering.

ROIC averaged 18.9% over the decade and reached 23.3% in FY2025. In every year of the available record, ResMed earned returns materially above its estimated cost of capital, a consistency that is more impressive than any single-year figure.

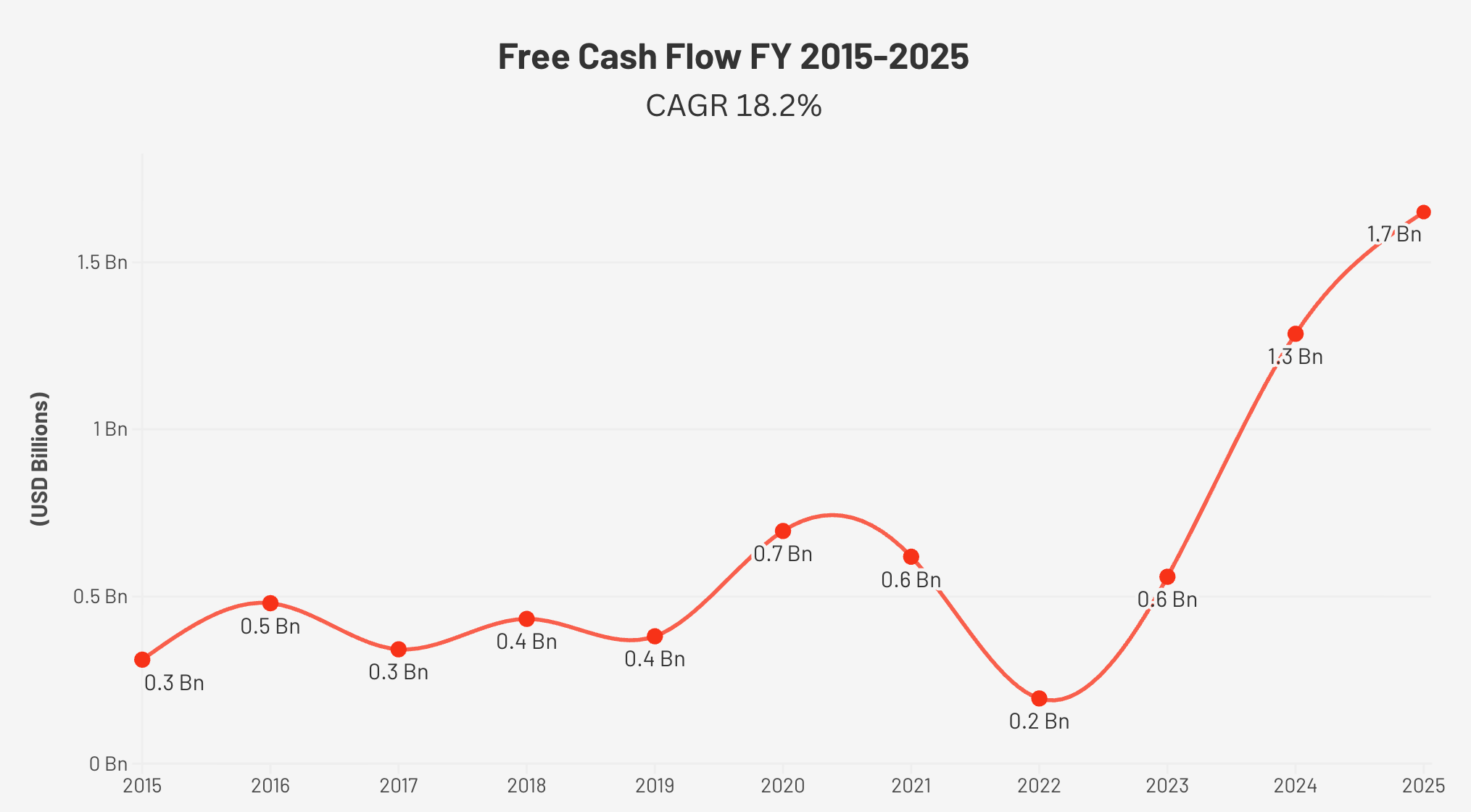

Free Cash Flow, the Real Story

Free cash flow (FCF) grew from $311M in FY2015 to $1,651M in FY2025, a 5.3x increase at an 18.2% CAGR. There was one significant dip: FY2022, when FCF collapsed to $195M despite strong revenue. The cause was working capital. The Philips recall demand surge required ResMed to draw down inventories and then rapidly rebuild them, creating a large transient cash outflow. Simultaneously, an elevated FY2021 effective tax rate of 46.3%, driven by a one-time $200M charge related to pre-acquisition earnings, further compressed cash in that period. Both were temporary. FCF recovered to $559M in FY2023, $1,286M in FY2024, and $1,651M in FY2025.

The FCF margin of 32.1% in FY2025 is the highest in the company’s history. Capex (capital expenditure) as a percentage of operating cash flow has fallen from 19% in FY2015 to just 6% in FY2025, reflecting the asset-light nature of a platform built primarily on software, data, and intellectual property rather than physical infrastructure.

Balance Sheet

Cash and equivalents stood at $1.21 billion at June 30, 2025, against total debt of approximately $670M, producing a net cash position of roughly $540M. Debt-to-equity has improved dramatically from the 0.38 reading in FY2023 (following the MEDIFOX DAN acquisition) to 0.14 at year-end FY2025. The revolving credit facility of $1.5 billion remains fully undrawn, maturing in 2027.

One genuine weakness worth naming: goodwill of $3.05 billion represents approximately 37% of total assets. This reflects the accumulated premium paid for acquisitions, primarily Brightree, Propeller Health, and MEDIFOX DAN. Tangible book value per share is substantially lower than reported book value. The intrinsic value of this business rests almost entirely on intangible assets, data, software, clinical relationships, regulatory approvals. That is a strength when the business performs and an accounting vulnerability if any major acquisition disappoints.

ResMed also pays a dividend of $2.12 per share in FY2025, representing a yield of approximately 0.95% at the current price, a signal of financial maturity that has grown steadily from $1.12 per share a decade ago.

4. Growth Levers

The Diagnosis Gap, the Single Biggest Lever

Here is the most important number in this entire report: fewer than 20% of OSA sufferers in the United States have been diagnosed and treated. In most international markets, the figure is closer to 10%.

ResMed does not need to take market share from anyone. It just needs the healthcare system to get better at finding the patients who already exist. Every percentage point improvement in diagnosis rates represents millions of people entering a care pathway that runs directly through ResMed’s ecosystem. This is the kind of structural growth driver that does not require macroeconomic tailwinds, product cycles, or competitive displacements. It just requires time.

ResMed is actively investing to accelerate this. NightOwl, a portable, cloud-connected, fully disposable diagnostic device that measures OSA severity overnight without requiring a clinic visit, launched across the US in April 2025. The acquisition of VirtuOx, an independent diagnostic testing facility, in May 2025 further expands the company’s ability to bring diagnosis into the home. The goal is to compress the traditional pathway, specialist referral, sleep lab, equipment pickup, device initiation, into something much closer to a single session at home.

International Penetration, COPD, and Software

The international opportunity mirrors the domestic one, large, underpenetrated, and growing as clinical awareness spreads and reimbursement coverage expands. International Sleep and Breathing Health revenue grew 9% in FY2025, and this segment operates at a fraction of US penetration levels across most geographies.

COPD (Chronic Obstructive Pulmonary Disease) affects approximately 480 million people globally and is the world’s third leading cause of death. ResMed’s non-invasive ventilation (NIV) and high-flow therapy (HFT) products for COPD patients represent a growing segment that the revenue breakdown does not currently call out separately, but it is a meaningful adjacency that deepens the platform’s clinical reach beyond sleep.

Residential Care Software, currently sold only in the US and Germany, grew 10% in FY2025 to $641M. Geographic expansion of this segment is a medium-term option that has not yet been exercised.

5. Management

The Farrell Family and Long-Term Alignment

ResMed is, at its core, a founder-influenced business. Dr. Peter Farrell built ResCare from a single licensed technology in Sydney in 1989 and steered it to become the global leader in sleep therapy. His son Mick Farrell has served as CEO since 2013, presiding over the company’s transformation from a device manufacturer into a connected care platform.

The family maintains meaningful skin in the game. Mick Farrell holds approximately 0.32% of outstanding shares, valued at roughly $105M at current prices. Dr. Peter Farrell, as founder and board director, directly owns a further 60,773 shares. While institutional investors including Vanguard and BlackRock collectively own the majority of the company, the Farrell family’s retained ownership signals genuine long-term conviction rather than founders who cashed out at the earliest opportunity.

Mick Farrell’s compensation structure reinforces that alignment. Approximately 91-92% of his total pay is performance-based, stock awards and options tied to specific financial metrics including revenue growth and EPS. Base salary accounts for only about 8% of total compensation. This is the kind of structure I look for in management: the CEO is economically motivated by the same outcomes that matter to long-term shareholders.

His communication style has been consistently direct on difficult topics. When the GLP-1 (glucagon-like peptide-1) panic hit in mid-2023 and ResMed’s stock fell more than 30%, Farrell engaged with the clinical evidence head-on rather than deflecting. He presented ResMed’s own patient data on GLP-1 users, made the probability-weighted case for ongoing demand, and continued investing in the business rather than cutting costs to manage short-term numbers. That is the kind of management behaviour that matters over a full market cycle.

Capital Allocation

R&D (Research and Development) spending of $331M in FY2025, representing 6.4% of revenue, has been sustained consistently across the decade. This is the right posture for a business whose competitive position depends on staying ahead clinically and technically.

On acquisitions, the track record is mixed but acceptable. Brightree has been clearly value-creating, it transformed ResMed from a device company into a platform company with deep provider relationships. The MEDIFOX DAN acquisition at approximately EUR 975M in FY2023 is too early to assess definitively, though integration appears to be progressing. The Propeller Health acquisition in FY2019 at $225M has been harder to evaluate but is smaller in scale.

Shareholder returns have grown steadily: dividends increased from $1.12 to $2.12 per share over the decade, and buybacks of $300M were executed in FY2025. Together with dividends, that represents approximately 37% of FCF returned to shareholders, the remainder retained for investment. I find that balance reasonable given the available organic growth runway.

6. Valuation

What the Market Is Pricing In

At $224 per share, I estimate the market is pricing ResMed at approximately 23 years of discounted future cash flows. My valuation framework expresses price as the number of years of a company’s future cash flows, discounted at an appropriate rate, that are already embedded in today’s price. The assumptions I use are consistent with the company’s current and historical operating performance. Nothing heroic, nothing pessimistic.

23 years puts ResMed in the Hold zone.

To be direct about what that means for me: I don’t initiate new positions in the Hold zone. The Bearhold framework is built around the idea that when you are buying a stake in a business, you want the price working in your favour, not just the fundamentals. The Attractive zone (16–20 years) and the Exceptionally Attractive zone (below 15 years) are where I look to deploy capital. At those levels, the price embeds significantly less of the company’s future than the business’s quality justifies, and an investor captures both the fundamental compounding and the valuation correction as it plays out.

At 23 years, I am essentially paying a fair price for quality I can see clearly. The fundamentals of this business are genuinely exceptional, but there is limited margin of safety in the entry price. Every dollar of return has to be earned through the business’s ongoing performance, there is no valuation tailwind to help.

What I Am Waiting For

ResMed becomes interesting to me as a new position somewhere in the Attractive and the Exceptionally Attractive zones. That does not happen often for businesses of this quality. It tends to happen when the market becomes temporarily preoccupied with a specific risk, a GLP-1 study result, a reimbursement cut, an earnings miss driven by inventory timing, and the stock reprices faster than the underlying business warrants.

7. Risks

The GLP-1 Question

Since mid-2023, the dominant narrative around ResMed has been the GLP-1 risk. Glucagon-like peptide-1 agonist drugs, Ozempic, Wegovy, Zepbound and others, cause significant weight loss in a meaningful proportion of users, and obesity is a primary driver of OSA in a large patient population. If these drugs reduce OSA prevalence materially, the argument goes, ResMed’s addressable market shrinks.

The clinical evidence is real. The FDA approved tirzepatide (Zepbound) in December 2024 specifically for the treatment of moderate-to-severe OSA in adults with obesity, after clinical trials demonstrated meaningful reductions in apnea-hypopnea index among treated patients.

I take this risk seriously. But I believe it is more limited than the 2023 market reaction implied, for three reasons.

First, OSA is not purely mechanical. The condition has neurological and anatomical components, airway geometry, muscle tone, neural respiratory drive, that weight loss does not fully resolve. ResMed’s own connected patient data shows that a meaningful proportion of GLP-1 users who achieve significant weight reduction continue to require CPAP therapy.

Second, the undiagnosed population dwarfs the treated population. The 80% of OSA sufferers who have never received a diagnosis are entering the care pathway as awareness grows. This demand source is entirely independent of GLP-1 penetration.

Third, real-world GLP-1 adherence is substantially lower than clinical trial completion rates. Weight regain is common on discontinuation. Access constraints, particularly outside developed markets, further limit penetration.

This is a risk that deserves ongoing monitoring, particularly as longer-duration GLP-1 data accumulates. It is not a reason to avoid the business; it is a reason to track it carefully and incorporate it into the price I am willing to pay.

Reimbursement and Policy Risk

A meaningful portion of ResMed’s revenue flows through Medicare, Medicaid, and private insurers. The US DMEPOS (Durable Medical Equipment, Prosthetics, Orthotics and Supplies) Competitive Bidding Program has historically placed downward pressure on Medicare reimbursement rates. CMS (Centers for Medicare & Medicaid Services) rate changes and ACA (Affordable Care Act) enrollment policy are ongoing headwinds. The recently enacted One Big Beautiful Bill Act makes changes to Medicaid funding and ACA enrollment that could reduce the insured patient population over time, though the specific effect on sleep therapy demand remains uncertain.

This is a persistent risk that ResMed has navigated through multiple policy cycles. It acts as a headwind to pricing power but has not historically disrupted the underlying demand trajectory.

Goodwill and Acquisition Risk

Goodwill of $3.05 billion, 37% of total assets, reflects the cumulative premium paid for acquisitions. The MEDIFOX DAN acquisition at approximately EUR 975M is the largest and most recent at scale. If integration underdelivers, or if the German software market dynamics shift unfavourably, a material impairment charge would hit reported equity significantly. This is the honest weakness in an otherwise strong balance sheet.

Tariffs and Supply Chain

ResMed manufactures primarily in Australia and Singapore. The tariff environment as of early 2025 has created some input cost uncertainty, though medical device tariff relief has been confirmed through US Customs as of the FY2025 filing date. The situation remains dynamic and worth monitoring.

What Would Change My Mind?

If GLP-1 clinical data continues to accumulate showing high real-world adherence and sustained OSA resolution, not just single-study results, that would require a fundamental reassessment of the long-term volume outlook. If operating margins begin contracting despite revenue growth, that signals competitive pricing pressure and potential moat erosion. If a major acquisition integrates poorly or requires a goodwill writedown, that is a capital allocation warning I would take seriously.

8. The Verdict

ResMed is one of the clearest examples of a business with genuine, compounding structural advantages. The data platform took thirty years to build. The installed base generates recurring revenue that grows with each diagnosis. The software layer makes providers sticky. The clinical evidence is deep and growing. And the addressable market, driven by the vast undiagnosed population, has decades of runway left.

The financial record across ten years confirms the quality: revenue tripled, operating margins expanded by 8.4 percentage points, ROIC averaged 18.9%, and free cash flow grew fivefold. This is what a durable competitive advantage looks like in the numbers.

The GLP-1 risk is real. The goodwill load deserves monitoring. Reimbursement policy is a persistent headwind. These are honest weaknesses and they belong in any fair assessment of the business.

ResMed is Approved in the Bearhold Universe. It sits in the Hold zone at the time of this publication. I am not buying today. But if the price moves into the Attractive zones, whether through a market correction, a temporary earnings disruption, or another episode of fear about a risk the market overstates, I will be ready to act.

Disclaimer: This report reflects the author’s personal views and is not an investment advice. Investing carries the risk of permanent capital loss. Read the full disclaimer here

The author does not currently hold a position in $RMD at the time of publication.

Sources

ResMed Inc. Form 10-K, Fiscal Year Ended June 30, 2025 (filed August 8, 2025)

ResMed Inc. Form 10-K, Fiscal Year Ended June 30, 2024 (filed August 9, 2024)

GuruFocus Financial Database — ResMed (NYSE: RMD), extracted April 4, 2026

GuruFocus Financial Database — Philips (NYSE: PHG), extracted April 5, 2026

Philips Annual Reports 2020–2025

Lancet Respiratory Medicine (2019): “Estimation of the global prevalence and burden of obstructive sleep apnoea”

FDA Drug Approval: Tirzepatide (Zepbound) for OSA, December 2024

ResMed Press Releases: NightOwl US launch (April 2025); VirtuOx acquisition (May 2025)

CMS DMEPOS Competitive Bidding Program documentation

ResMed Proxy Statement (DEF 14A), filed October 2025 — executive compensation and insider ownership