Under The Hood, Novo Nordisk A/S ($NVO)

Company Analysis & Valuation

The Outlook

There is a hormone produced in the human gut after you eat. It signals to your brain that you have had enough. It slows the stomach from emptying. It tells the pancreas to release insulin. For most of medical history, this hormone, glucagon-like peptide-1, or GLP-1, was just a footnote in endocrinology textbooks. Then a Danish pharmaceutical company spent thirty years studying it, synthesising molecules that mimic it, extending their half-life in the bloodstream from a few minutes to a full week, and iterating on the formulation until they could put it in a once-weekly injection. And then, remarkably, into a pill.

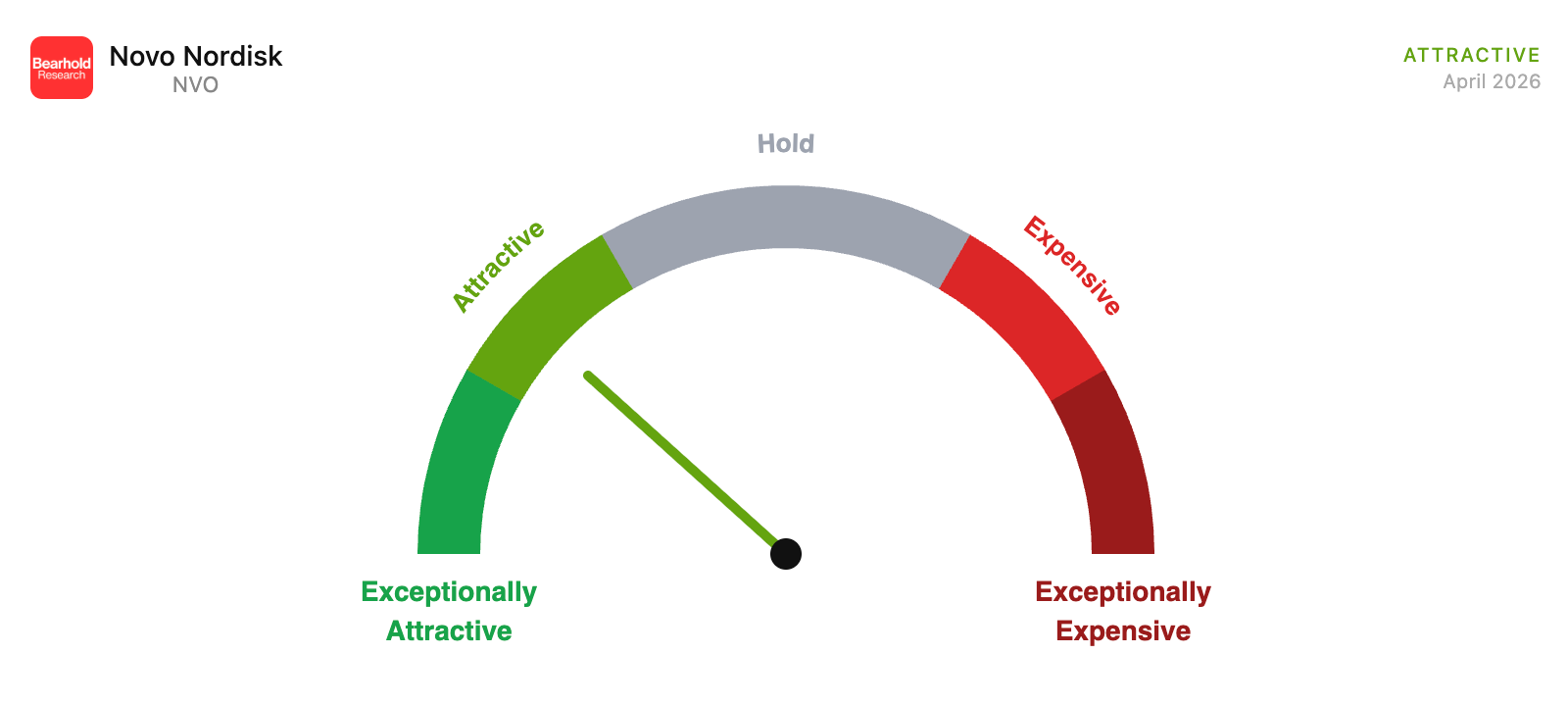

What Novo Nordisk has built is not just a drug franchise. It is a century-old institution that made the right scientific bet at the right moment in history, and found itself at the centre of what may be the most commercially significant pharmacological development of our generation. GLP-1 drugs are not a weight loss trend. They are a reclassification of obesity from a lifestyle problem to a treatable chronic disease, and Novo Nordisk is the company that did the reclassifying. My valuation framework puts the stock at 17 years of embedded discounted cash flows, firmly in the Attractive zone.

The business is on the Bearhold Watchlist, not yet Approved, and this report explains the distinction.

At a Glance

Company: Novo Nordisk A/S

Ticker: NVO · NYSE / NOVO B · Nasdaq Copenhagen

Sector: Healthcare

Industry: Pharmaceuticals

Market Cap: ~$168 billion

Dividend Yield: ~4.8% (price $37.5)

Current Stock Price: $37.50

First Coverage: April 2026

Bearhold Universe Status: Watchlist

Valuation Zone: Attractive (last updated April 2026)

This report reflects the author's personal views and does not constitute investment advice. Investing carries the risk of permanent capital loss. The author held a position in NVO during the research process and exited prior to publication. No position is held at the time of publishing. Read the full disclaimer here

1. The Business

From Insulin to the Drug That Changed Everything

The story of Novo Nordisk starts in 1923, the same year insulin was first commercially produced, just two years after its discovery in Canada. A group of Danish scientists recognised that this life-saving hormone would need to be manufactured reliably, at scale, for the millions of people with type 1 diabetes who would otherwise die without it. They built a small laboratory in Copenhagen and began producing insulin from pig and cow pancreas. That business became Novo Nordisk.

For most of the 20th century, the company’s identity was simple: it made insulin. Its early products were animal-derived insulins, extracted directly from livestock pancreas. These worked, but they were not identical to human insulin, which meant the body sometimes rejected them. In the 1980s, Novo Nordisk was among the first companies to produce human insulin through recombinant DNA technology, meaning scientists could engineer bacteria to produce an exact replica of the human molecule. This was a step-change in treatment quality and marked the company’s transition from a manufacturer to an innovator.

Through the 1990s and 2000s, the company developed long-acting insulins, versions that are released slowly into the bloodstream over 24 hours, eliminating the need for multiple daily injections. Tresiba (insulin degludec), one of Novo Nordisk’s flagship insulins, is a once-daily injection that lasts over 40 hours, offering far more flexibility than older formulations. These innovations matter because the management of type 2 diabetes, which affects roughly 500 million people globally, traditionally relied entirely on insulin injections. The more convenient and precise those injections became, the more patients could comply with treatment, and the better their outcomes.

The GLP-1 Discovery

In the 1980s, researchers discovered that the intestinal hormone GLP-1 had remarkable properties: it stimulated insulin release only when blood sugar was elevated, suppressed glucagon (the hormone that raises blood sugar), and slowed digestion. Unlike insulin, which works regardless of blood sugar levels and can cause dangerous hypoglycaemia (dangerously low blood sugar) if dosed incorrectly, GLP-1 had a built-in safety mechanism. It only worked when it was needed.

The problem was that natural GLP-1 is destroyed in the bloodstream within a few minutes. To be useful as a drug, scientists needed to create a version that lasted long enough to have a therapeutic effect. This is where Novo Nordisk’s decades of molecular engineering experience paid off. Their scientists modified the GLP-1 molecule to make it resistant to the enzyme that breaks it down, and bound it to a carrier protein to extend its life in the body. The result was semaglutide, a once-weekly injectable that mimics GLP-1 with dramatically extended duration.

The Same Drug, Different Names

This is one of the most frequently misunderstood aspects of Novo Nordisk’s business, so I want to explain it clearly.

Ozempic and Wegovy contain the exact same active ingredient: semaglutide. The difference is the dose. Ozempic, approved for type 2 diabetes, is available at doses of 0.5mg and 1mg per week. Wegovy, approved for obesity, is dosed at 2.4mg per week. Rybelsus is the oral version of semaglutide, available in daily pill form at doses of 7mg and 14mg, approved for diabetes. The Wegovy pill, approved by the FDA (US Food and Drug Administration) in January 2026, is an oral version for obesity at 25mg per day.

The reason these identical molecules have different names is both regulatory and commercial. Regulatory agencies approve drugs for specific indications at specific doses, a company cannot simply sell its diabetes drug off-label for obesity without a separate approval process. More importantly, it is commercial. Insurance companies in the US have historically refused to cover obesity as a disease, meaning they will reimburse Ozempic for a diabetic patient but not Wegovy for an obese patient who does not have diabetes, even though the molecule is the same. By separating the brands, Novo Nordisk can price and position each product for its specific reimbursement channel. Ozempic’s lower dose and diabetes indication gives it a clearer path to insurance coverage. Wegovy’s obesity approval opens a different, harder, but rapidly expanding reimbursement channel.

Why GLP-1 Is Replacing Traditional Insulin Therapy

The conventional treatment pathway for type 2 diabetes used to look like this: start with oral medication (metformin), add more oral medications as the disease progresses, and eventually transition to daily insulin injections as the pancreas loses its ability to produce enough insulin on its own. Patients often spent years on multiple medications and ended up injecting insulin multiple times daily, managing complex carbohydrate intake, and still experiencing high rates of cardiovascular disease, kidney disease, and nerve damage.

GLP-1 drugs changed this trajectory. Clinical trial after clinical trial showed that semaglutide not only controlled blood sugar as effectively as insulin but also reduced body weight, lowered blood pressure, reduced inflammation, and, critically, reduced cardiovascular mortality. The SELECT trial, completed in 2023, showed that Wegovy reduced major adverse cardiac events such as heart attack and stroke by 20% in people with obesity and established cardiovascular disease. The FLOW trial showed Ozempic reduced the progression of chronic kidney disease by 24%. These are outcomes that insulin, despite decades of use, has never convincingly demonstrated.

The result is that GLP-1 drugs are no longer just an add-on to diabetes therapy. They are increasingly the first-line treatment, with insulin reserved for patients who cannot tolerate GLP-1 drugs or whose disease has progressed beyond what GLP-1 can manage. This is why Novo Nordisk’s older insulin products, Victoza, Levemir, are declining. Victoza sales fell 43% in constant currency terms in FY2025. These are not accidents. They are the natural consequence of a superior drug replacing its predecessor.

How a Diabetes Drug Became the Defining Weight Loss Treatment

The weight loss effect of GLP-1 drugs was noticed early in clinical trials but treated initially as a side effect. Patients taking these drugs for diabetes were losing significant body weight, not through stimulant effects, but because the brain was receiving genuine satiety signals, reducing appetite naturally. Novo Nordisk’s scientists understood what this meant: there was a separate, enormous market here.

The STEP trials, completed in 2021, tested semaglutide 2.4mg specifically for obesity in people who did not have diabetes. Participants lost an average of 14.9% of their body weight. That may sound modest, but in the context of obesity pharmacology, where most approved drugs had achieved 3–5% weight loss at best, it was extraordinary. The FDA approved Wegovy in June 2021, and the obesity treatment market was never the same.

Today the business operates across three segments. Obesity care generated DKK 82.3 billion in FY2025, up from essentially zero in 2019, when it barely existed as a category, growing 31% at CER (constant exchange rates). Diabetes care generated DKK 207.1 billion, growing 4% at CER. Rare disease, treatments for growth hormone disorders and haemophilia, generated DKK 19.6 billion, growing 9% at CER. Total revenue reached DKK 309 billion in FY2025, up from DKK 157.5 billion five years earlier.

2. The Moat

What Makes This Business Hard to Compete with

Novo Nordisk’s competitive position rests on four reinforcing pillars, and understanding each one is important before looking at the financial results.

The first is molecular depth. Semaglutide has been in development since the early 2000s and has accumulated a clinical evidence base that no competitor can replicate quickly. Cardiovascular outcomes trials take five to seven years to complete and cost hundreds of millions of dollars. Novo Nordisk has completed the SELECT trial for obesity, the SUSTAIN-6 trial for diabetes, and the FLOW trial for kidney disease. These are not marketing claims, they are data sets generated from tens of thousands of patients over years. A new entrant today, even with a technically equivalent molecule, would need to spend a decade and billions of dollars to generate comparable evidence. That is structural protection.

The second is manufacturing expertise. GLP-1 drugs are biologics, they are not simple chemical compounds. They are produced through complex biological processes that require precision at every step, from fermentation to purification to formulation for injection or oral delivery. The development of a stable oral semaglutide formulation, which required solving the problem of getting a large peptide molecule through the stomach without being destroyed, is a technical achievement that took years of R&D investment. The current DKK 60 billion annual capital expenditure is explicitly aimed at expanding this infrastructure. It takes time and expertise that cannot be purchased overnight.

The third is commercial infrastructure. Novo Nordisk has one of the deepest specialist sales forces in pharmaceutical history, built over a century of selling to endocrinologists and diabetologists. These relationships are not purely transactional, prescribers who have spent fifteen years trusting Novo Nordisk’s insulin products were natural early adopters of Ozempic. That trust transfers, and it creates a distribution advantage that is invisible in the financial statements but profoundly real.

The fourth is patient stickiness. GLP-1 drugs require continued use to maintain their effect, body weight returns on discontinuation, and blood sugar control deteriorates. This means a patient who starts on Ozempic or Wegovy is, in practice, a recurring revenue stream. It is not a perfect annuity, discontinuation rates are real and I will discuss them in the Risks section, but the baseline adherence creates a revenue durability that few pharmaceutical franchises can match.

The empirical evidence of the moat is in the margins. The operating margin has ranged from 41.3% to 45.8% across every year from 2015 to 2025, averaging 43.1% over the decade. A business that is losing its competitive position does not sustain margins at that level across ten years of significant disruption, including pricing pressure from biosimilars on older products, a global pandemic, supply constraints, and a complete transformation of the revenue mix.

3. The Paradox at the Heart of the Business

One Company Treating the Same Disease it is Helping Prevent

I want to pause on something that I have not seen discussed clearly enough in most analyses of Novo Nordisk. It is a genuine strategic tension at the heart of the business model, and it deserves honest examination.

Novo Nordisk sells two categories of products. In the diabetes segment, it sells drugs that treat and manage diabetes, products that patients typically use for life, generating stable, recurring revenue. In the obesity segment, it sells drugs that cause significant weight loss, and we now have substantial evidence that sustained weight loss reverses or prevents type 2 diabetes in a meaningful share of patients.

I do not think this resolves neatly. Here is how I think about it.

In the near term, the two businesses are growing simultaneously and serve largely different patient populations. Most Ozempic patients are type 2 diabetics with established disease. Most Wegovy patients are obese without a diabetes diagnosis. The overlap exists but it is not yet the dominant dynamic.

In the medium term, say five to ten years, if GLP-1 drug adoption reaches a meaningful share of the obese population, and if adherence rates are sustained, we should expect a measurable reduction in the incidence of new type 2 diabetes cases. This is good for society and genuinely good for patients. For Novo Nordisk’s diabetes franchise, it means the pool of newly diagnosed type 2 diabetics will eventually shrink. At the same time, the surviving diabetes franchise will treat a patient population with more advanced and complex disease, the patients for whom lifestyle intervention and GLP-1 therapy alone were not enough.

In the long term, the company’s own strategic positioning tells you what management believes: obesity care is the growth engine of the next decade, and diabetes care is the stable cash-generating foundation. The restructuring announced in FY2025, redirecting DKK 8 billion in annualised savings toward obesity and diabetes innovation, confirms this. They are not treating this as a zero-sum game within the portfolio. They are betting that the obesity market is large enough to more than offset any erosion in the diabetes base.

I think this is probably correct, but I hold it with appropriate uncertainty. The honest risk is that if obesity drugs penetrate much faster and at much higher adherence rates than current models project, the diabetes franchise could decline faster than the obesity franchise grows. I do not think this is the base case, the sheer scale of the undiagnosed and untreated obesity population is simply enormous, but it is the kind of second-order risk that deserves a place in any serious analysis of this business.

This unresolved dynamic is one of the reasons the obesity franchise has not yet earned the Approved designation, the long-term interaction between these two segments is genuinely uncertain in ways that a decade of insulin history was not.

4. Financial Performance

A Decade in Numbers

The ten-year financial record of Novo Nordisk is, on almost every metric except one, exceptional.

Revenue grew from $15.7 billion in FY2015 to $48.5 billion in FY2025, a compound annual growth rate of approximately 11.9% over ten years. The growth was not linear. Through 2021, the diabetes franchise expanded steadily. Then the GLP-1 obesity inflection arrived: from 2022 onwards, the company added roughly seven to nine billion dollars of revenue per year. The 2025 figure is more than three times the 2015 base.

Diluted EPS grew from $0.99 in FY2015 to $3.61 in FY2025, a compound annual growth rate of 13.8%. This is the number I trust most as a proxy for earnings power, because it is clean, consistent, and not distorted by the current capex cycle. The share count declined from 5,155 million to 4,448 million over the decade, a consistent buyback programme that reduces the per-share denominator. Dividends per share grew from $0.37 in 2015 to $1.82 in 2025.

The gross margin averaged approximately 83.9% from 2015 through 2025, near the pharmaceutical ceiling, reflecting proprietary manufacturing and durable pricing power. In FY2025, gross margin fell to 81.0%. This is a real and material decline, driven primarily by the enormous surge in cost of goods sold as the company scaled manufacturing rapidly and absorbed restructuring costs related to facility consolidation.

The operating margin has ranged from 41.3% to 45.8% across every year of the decade, averaging 43.1%. FY2025 came in at 41.3%, adjusted for the DKK 8 billion restructuring charge (In September 2025, Novo Nordisk announced a “company-wide transformation” involving approximately 9,000 job cuts, this resulted in a one-off DKK 8.0 billion restructuring cost), underlying operating profit grew 13% at constant exchange rates, and the reported operating margin would have been meaningfully higher. The consistency of margins at this level across ten years of significant business model change is one of the most powerful signals of competitive quality I have seen in this type of analysis.

ROIC (return on invested capital) was 73.4% in FY2015 and declined to 26.8% in FY2025 as the capital base expanded with the manufacturing buildout. The directional decline is expected, the denominator grew faster than the numerator as capital was deployed into assets not yet generating returns. The absolute level of 26.8% is still exceptional for a business of this scale. Eli Lilly’s ROIC reached 33% in FY2025 after a decade of expansion from 10.9% in 2015. The two companies are converging at the high end of the global pharmaceutical industry.

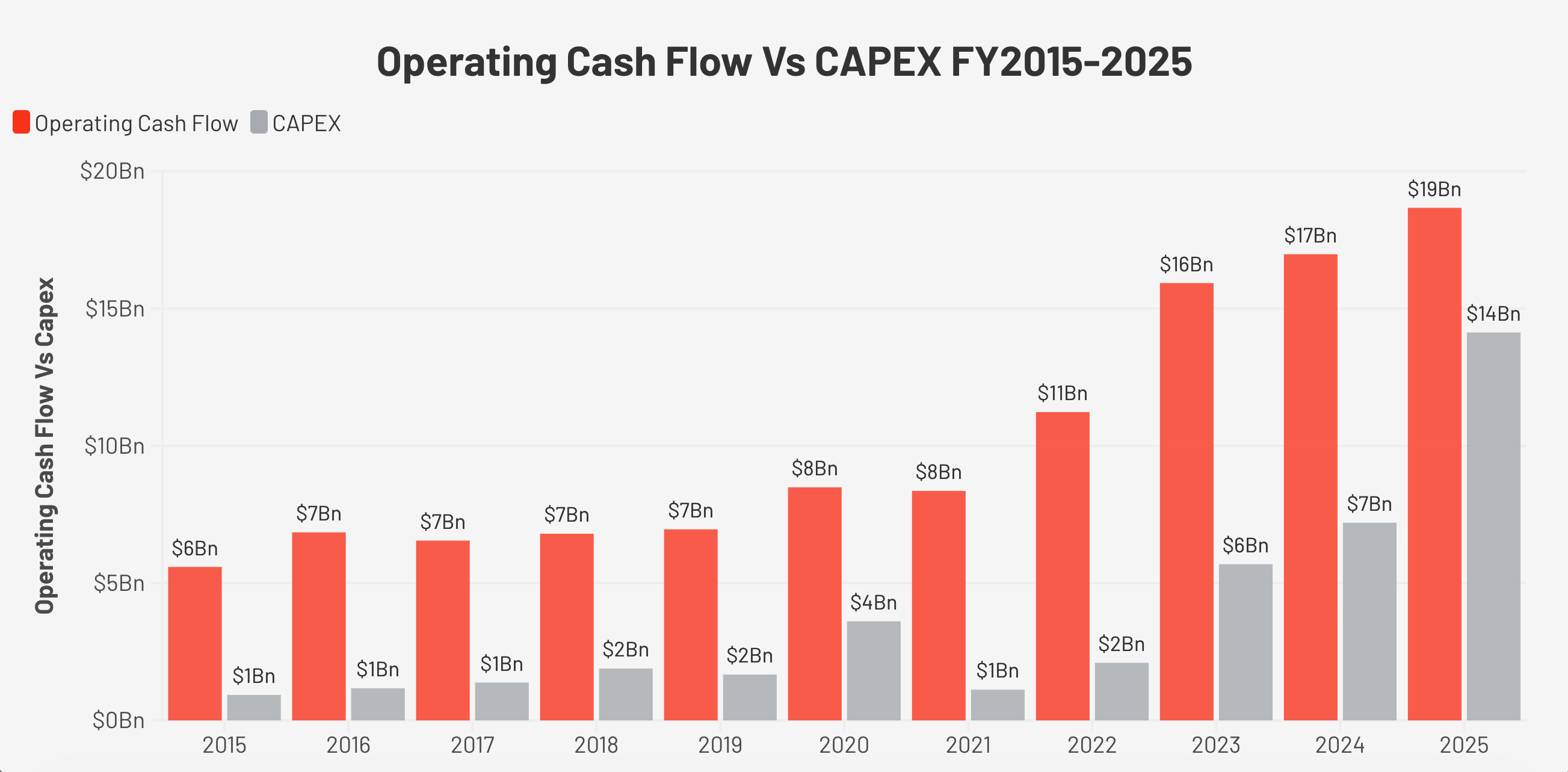

The FCF Story, Why the Headline Number is Not the Full Story

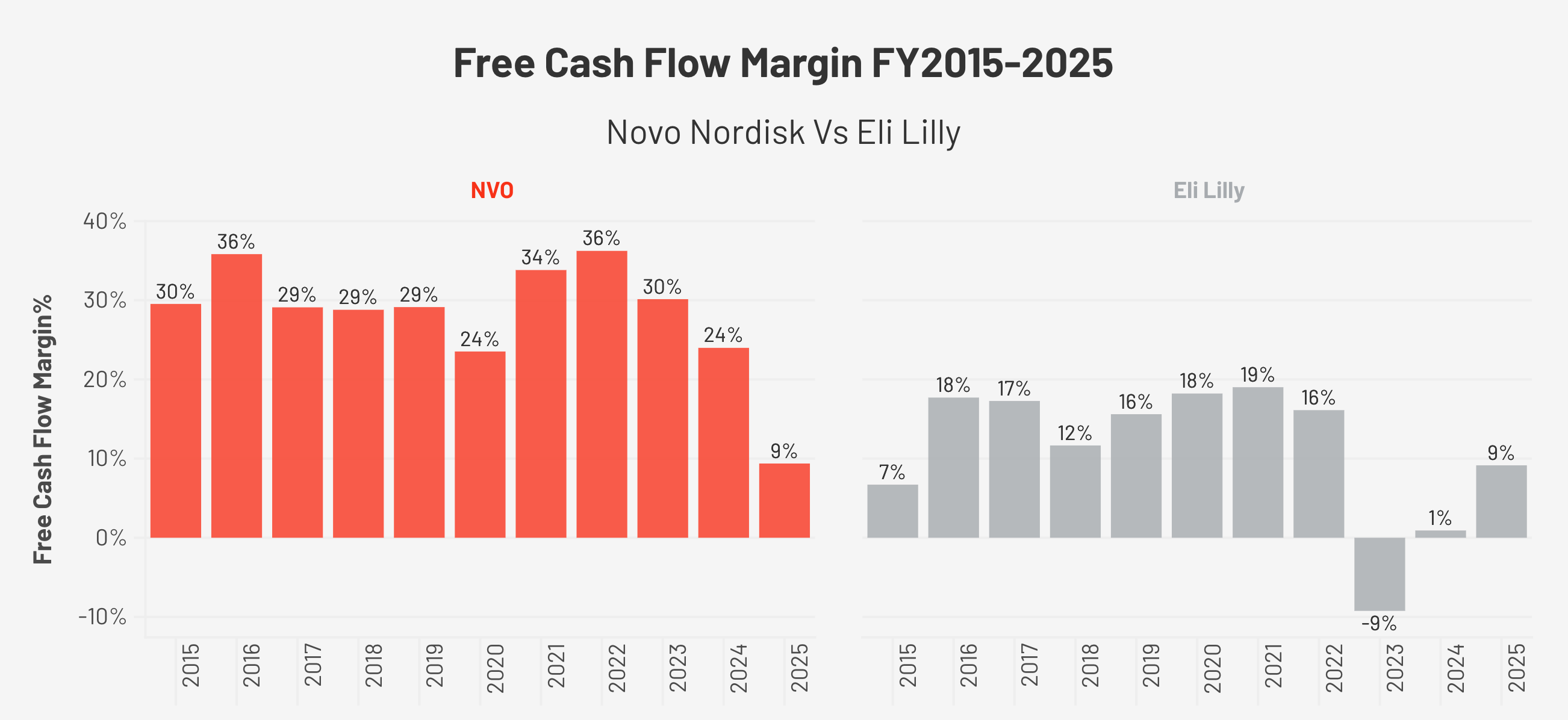

Free cash flow (FCF: cash left after all operating expenses and capital investment) was remarkably stable from 2015 through 2023, growing from $4.7 billion to $10.2 billion. OCF (operating cash flow: cash generated from the business before investment) margins throughout this period ranged from 35% to 47%, and FCF margins ranged from 24% to 36%.

In FY2025, FCF collapsed to $4.5 billion, a margin of 9.4%, compared to a ten-year average of approximately 28%.

The cause is entirely capital expenditure. Capex (spending on factories and equipment) was $935 million in FY2015, representing 17% of OCF. By FY2025, it had reached $14.1 billion, 76% of OCF. The company spent DKK 60 billion on property, plant, and equipment in FY2025, principally to build manufacturing capacity for GLP-1 drugs.

The important distinction is that OCF margins remained within historical norms: 38.5% in FY2025. The business is not generating less cash from its operations, it is reinvesting aggressively in infrastructure. Because FCF per share is temporarily distorted, I use EPS as my primary earnings proxy throughout this report. The operating health of the business is intact.

The Balance Sheet Has Changed

Debt-to-equity was 0.02x in FY2015, essentially no debt. By FY2025, it had risen to 0.68x. The company now carries meaningful net debt, having taken on borrowings to fund both the manufacturing buildout and several acquisitions, including the Catalent manufacturing sites that Novo Holdings purchased in 2024 for $11.7 billion and subsequently deployed to Novo Nordisk’s production. This is manageable at current earnings levels, but it represents a structural shift from the near-pristine balance sheet that characterised this company through most of the last decade.

5. Regional Breakdown

The Numbers by Region (FY2025)

The detailed revenue data from the FY2025 annual report tells a story that the headline figures do not.

US Operations generated DKK 173.2 billion in total sales in FY2025, growing 3.4% as reported (8% at CER). Within that, Wegovy in the US generated DKK 51 billion, up from DKK 45.8 billion in 2024. Ozempic US sales were DKK 88.5 billion. These are extraordinary numbers for two products that barely existed five years ago.

International Operations generated DKK 135.9 billion, growing 10.5% as reported (14% at CER). The breakdown within International Operations reveals where the real opportunity sits:

EUCAN (Europe and Canada) generated DKK 66.1 billion, growing 14.9% as reported (16% at CER). Wegovy in EUCAN generated DKK 15.4 billion, up from DKK 7.7 billion in 2024, a doubling in a single year. This is what the early phase of a proper launch looks like. Europe is roughly two years behind the US in GLP-1 obesity adoption, constrained by more conservative payer systems and slower reimbursement approvals. The trajectory is clear.

Emerging Markets (mainly Latin America, Middle East, and Africa) generated DKK 30.4 billion, growing 3.1% as reported (8% at CER). Wegovy in Emerging Markets generated DKK 6.1 billion in FY2025, up from DKK 2.7 billion in 2024. This is one of the most interesting long-term opportunities and one of the most underdiscussed. Obesity prevalence in Latin America and the Middle East is extremely high, Brazil, Mexico, and Saudi Arabia are among the most obese nations on earth. The barrier is affordability and reimbursement coverage. As Novo Nordisk develops lower-cost formulations and access programmes, this market has a long runway.

APAC (Japan, Korea, Oceania, and Southeast Asia) generated DKK 20.7 billion, growing 18.8% as reported (25% at CER). Wegovy in APAC generated DKK 5.8 billion, up from DKK 1.9 billion in 2024, a tripling in a single year. Japan and South Korea have both launched Wegovy relatively recently, and the cultural and clinical context is different from the West. Japanese patients tend to be obese at lower BMI (body mass index) thresholds than Western patients, and the regulatory framework for obesity treatment has historically been restrictive. As awareness grows and reimbursement expands, APAC represents a meaningful expansion opportunity.

Region China generated DKK 18.7 billion, growing 0.8% as reported (5% at CER). This is the most complicated region, and I will address it directly in the Risks section. Wegovy in China generated DKK 796 million, still a very small number relative to the scale of the opportunity. China has a massive obesity and diabetes burden, but the semaglutide active ingredient patent expires there in 2026, which means low-cost domestic biosimilar competition is coming. The next two to three years in China will be a test of brand loyalty versus price.

The Global Penetration Opportunity

Here is the number I keep coming back to: the World Health Organization estimates approximately 890 million adults globally have obesity. Current GLP-1 treatment penetration is in the low single digits. The United States has an obesity prevalence of roughly 42% in adults, and fewer than 6% of eligible patients are currently on a branded GLP-1 drug. Even after the explosive growth of the last three years, the penetration story is genuinely in its early chapters.

6. Competition: Novo Nordisk vs. Eli Lilly

The Duopoly That Defines the GLP-1 Market

Novo Nordisk and Eli Lilly together represent the vast majority of commercial GLP-1 (glucagon-like peptide-1) prescriptions globally. No other company is remotely close to their combined scale in either diabetes or obesity. Understanding how these two businesses compare is essential.

Novo Nordisk pioneered this market. It was the first to achieve large-scale commercial success with semaglutide, the first to build a manufacturing infrastructure capable of supplying tens of millions of patients globally, and the first to bring an oral GLP-1 pill for obesity to market. That first-mover advantage is real and it matters, both commercially and in terms of the clinical evidence base accumulated across cardiovascular disease, kidney disease, and liver disease.

But Eli Lilly has overtaken Novo Nordisk in prescription market share, and that shift deserves honest acknowledgment. By the third quarter of 2025, Lilly held more than 57% of US monthly GLP-1 prescriptions across diabetes and obesity, with Novo Nordisk at approximately 43%, down from a position of clear leadership just two years earlier. The primary driver is tirzepatide, which activates two hormone receptors simultaneously, GLP-1 and GIP (glucose-dependent insulinotropic polypeptide), compared to semaglutide’s one. In Lilly’s SURMOUNT-1 trial, tirzepatide produced average weight loss of approximately 21–22% at the highest dose, compared to semaglutide’s 15% in the STEP trials. When a drug delivers meaningfully better efficacy and is available in adequate supply, prescribers and patients notice. Lilly’s 2026 revenue guidance projects approximately 27% growth. Novo Nordisk’s 2026 guidance is for negative adjusted sales growth at constant exchange rates. The divergence in near-term momentum is real and not easily dismissed.

Where It Gets More Complicated — The Pill Battle

The injectable competition is clear: Lilly leads on efficacy. But the oral market, which is where the next major wave of GLP-1 adoption is likely to come from, driven by patients who have consistently refused injections, is a more nuanced picture, and one that has shifted meaningfully in Novo Nordisk’s favour in just the past two weeks.

Novo Nordisk’s Wegovy pill was approved by the FDA in December 2025 and reached over 600,000 US prescriptions in its first few weeks. On April 1, 2026, 12 days before this report, the FDA approved Eli Lilly’s oral GLP-1, orforglipron, now branded as Foundayo. The pill competition is now live and direct.

The initial market framing was that Novo had first-mover advantage but Lilly had a convenience edge: Foundayo is a small-molecule drug that can be taken at any time with or without food, while the Wegovy pill is a peptide that requires a 30-minute fast each morning. For patients who already struggle with daily medication adherence, that restriction was seen as a meaningful disadvantage for Novo.

Then, on April 2, 2026, one day after Foundayo’s approval, Novo Nordisk presented the ORION study at the Obesity Medicine Association’s annual conference in San Diego. The study used a population-adjusted indirect comparison of data from the OASIS 4 trial (Wegovy pill) and the ATTAIN-1 trial (Foundayo), and the results were notable. Oral semaglutide showed 3.2 percentage points greater weight loss than orforglipron on a real-world adherence basis. On tolerability, patients on orforglipron had approximately four times higher odds of discontinuing due to any adverse event, and nearly 14 times higher odds of discontinuing specifically due to gastrointestinal side effects. A separate patient preference survey of 800 adults found that 84% favoured the oral semaglutide profile over orforglipron, and 65% of those respondents said the morning fasting requirement would not significantly disrupt their daily routine.

I want to be clear about what this data is and what it is not. The ORION study is an indirect comparison across two separate trials, not a head-to-head study with identical protocols. The researchers themselves flagged substantial uncertainty in the tolerability findings, the confidence interval on the gastrointestinal discontinuation figure runs from 2.0 to 96.0, which is wide enough to counsel humility. The study was also funded and presented by Novo Nordisk, which means it should be read with appropriate critical distance even if the methodology is standard. No direct head-to-head trial between these two pills exists, and neither company is likely to fund one voluntarily.

With those caveats stated, the direction of the finding is meaningful. In a chronic disease drug that patients take daily for the rest of their lives, tolerability and real-world adherence matter more than any single efficacy number. A drug that patients stay on compounds its benefit over years and generates recurring revenue. A drug that patients are significantly more likely to discontinue due to side effects loses both the clinical benefit and the commercial durability. The convenience narrative that Lilly was relying on to offset Novo’s first-mover advantage in the oral market has been meaningfully complicated by this data.

The Margin and Balance Sheet Picture

On financial quality, Novo Nordisk maintains the structural advantage. Its gross margin averaged approximately 83.9% from 2015 through 2024, falling to 81.0% in FY2025, compared to Eli Lilly’s expansion from 74.8% in 2015 to 83.0% in FY2025. Lilly has only just reached the margin level that Novo Nordisk has sustained for a decade. Operating margins tell the same story: Novo Nordisk’s range of 41.3% to 45.8% throughout the decade versus Lilly’s expansion from 18% in 2015 to 45.6% in FY2025. Both companies are now experiencing the same capex-driven FCF (free cash flow) compression, Lilly’s FCF margin was 9.2% in FY2025 versus Novo Nordisk’s 9.4%, as both build manufacturing infrastructure for the same market opportunity. On leverage, Novo Nordisk is more conservatively capitalised at 0.68x debt-to-equity versus Lilly’s 1.60x.

One metric I flag for both companies is inventory. Eli Lilly’s Days Inventory Outstanding, a measure of how long products sit in inventory before being sold, increased from 196 days in FY2021 to 352 days in FY2025, nearly a doubling in four years. This could reflect pre-launch positioning or manufacturing buffer-building, but it is a number worth watching in future quarterly reports for signs of demand forecasting error.

The Summary

The injectable market: Lilly leads on efficacy with tirzepatide and has taken prescription share from Novo Nordisk. That is a fact.

The oral market: Novo Nordisk leads on efficacy and, based on the most current available data, leads on tolerability as well, though the evidence is indirect and requires a head-to-head trial to confirm definitively.

The financial quality: Novo Nordisk has the stronger historical margin profile and more conservative balance sheet.

The pipeline: Novo Nordisk’s CagriSema, filed for FDA approval in December 2025 with a decision expected around October 2026, produced 22.7% weight loss in the REDEFINE 1 trial, essentially matching tirzepatide’s injectable efficacy. If approved, it closes the injectable efficacy gap before Lilly’s next-generation retatrutide (a triple receptor agonist) reaches market.

I would describe the current state as a genuine competition between two exceptional businesses, with Lilly holding the commercial momentum in injectables and Novo Nordisk mounting a more credible defence in the oral market than the market appears to currently price in. The coming 18 months, CagriSema approval, head-to-head oral data if it emerges, and the real-world prescription trends between Wegovy pill and Foundayo, will determine whether Novo Nordisk’s defensive position stabilises or continues to erode. At $37.50, I believe the current price more than compensates for that uncertainty.

7. Growth Levers & Addressable Market

The Pipeline: Novo Nordisk’s Response to the Lilly Challenge

CagriSema is the most important near-term pipeline catalyst. It is a fixed-dose combination of cagrilintide (a long-acting amylin analogue, amylin is another satiety hormone produced by the pancreas) and semaglutide 2.4mg. In the REDEFINE 1 Phase 3 trial, participants lost an average of 22.7% of body weight assuming full adherence to treatment, and 20.4% on a real-world basis regardless of adherence. Both figures substantially exceed Wegovy’s current results. Novo Nordisk filed the NDA (new drug application) with the FDA in December 2025, and a decision is expected approximately October 2026.

Zenagamtide (amycretin), a single molecule that activates both GLP-1 and amylin receptors, is entering Phase 3 trials in 2026 in both injectable and oral forms, with early-phase data showing weight loss in the 20% range. The semaglutide 7.2mg dose achieved 20.7% weight loss and has received a positive opinion from the EMA (European Medicines Agency), with an FDA submission also filed. Wegovy was approved for MASH in the US in FY2025, MASH affects approximately 6% of the global population and has very limited approved treatment options, making this a meaningful new revenue channel.

The oral Wegovy pill, approved by the FDA in December 2025, is worth emphasising specifically. Injection hesitancy is a real and documented barrier to GLP-1 adoption. A meaningful share of patients who would benefit from these drugs decline or discontinue them because of the injection requirement. An oral formulation that achieved 16.6% average weight loss in trials, better than any previously approved oral obesity drug, removes that barrier entirely. This is a market expansion story, not just a market share story.

8. Management

Lars Fruergaard Jørgensen, Mike Doustdar, and a CEO Transition at a Critical Moment

Lars Fruergaard Jørgensen served as CEO from 2017 through August 2025. His tenure included the most transformative period in Novo Nordisk’s modern history, the pivot to obesity care, the launch of Wegovy, the extraordinary growth from 2021 to 2023, and the beginning of the current manufacturing buildout. On May 16, 2025, the company announced he would be stepping down following a period of market challenges and declining share price. On July 29, 2025, Mike Doustdar, then head of International Operations, was named as successor, with the formal handover taking place on August 7, 2025.

I read the transition thoughtfully. Jørgensen built the strategic architecture of the current business. Doustdar is, in many ways, the commercial architect of its execution: as head of International Operations, he oversaw the global Wegovy launch and was responsible for the market access strategy that determined how quickly the drug reached patients outside the US. His appointment is not a reversal of strategy. It is a shift in emphasis, from the scientific and strategic decisions of the build-out phase to the commercial and operational execution required to turn that investment into revenue.

The capital allocation record under the previous leadership is solid. Share count declined by approximately 14% over the decade through consistent buybacks. R&D (research and development) spending reached DKK 52 billion in FY2025, 16.8% of revenue, reflecting a genuine commitment to the pipeline rather than cost-cutting to protect near-term margins. The DKK 8 billion restructuring announced in FY2025, reducing the global workforce by approximately 9,000 positions, signals that management is willing to make uncomfortable structural decisions. I read that positively.

The governance structure deserves a note. Novo Holdings, controlled by the Novo Nordisk Foundation, holds approximately 77% of the voting rights through a dual-class share structure. This insulates management from short-term market pressure. It is a structural positive for a business with a multi-decade strategic horizon, though minority shareholders have limited influence over capital allocation decisions.

9. The Compounding Pharmacy Story

The GLP-1 compounding story is important context for understanding the FY2025 performance, and its resolution is one of the reasons I believe the near-term earnings trajectory is better than the FY2026 guidance implies.

When demand for Wegovy and Ozempic surged in 2022 and Novo Nordisk’s manufacturing could not keep pace, the FDA placed semaglutide on its official drug shortage list. Under US law, compounding pharmacies can produce copies of drugs on the shortage list. What followed was a large parallel market: an estimated 3.7 million Americans accessing compounded semaglutide through telehealth platforms at $150–$400 per month versus the $1,349 list price of Wegovy.

The FDA declared the shortage resolved on February 21, 2025. The legal basis for most large-scale compounding of semaglutide no longer exists. Courts sided with Novo Nordisk and the FDA in the key preliminary injunction hearings. As of September 2025, Novo Nordisk had filed 140 lawsuits and issued over 1,000 cease-and-desist letters against compounders. The management team acknowledged that the persistence of compounded semaglutide was a meaningful drag on branded volumes in 2025. As compounding recedes, that volume either transitions to branded Wegovy or is lost, but the channel overhang is clearing.

The TrumpRx Pricing Deal, Volume for Price

In November 2025, Novo Nordisk reached an agreement with the Trump administration under which Wegovy and Ozempic prices will be reduced to $350 per month through the TrumpRx government portal, down from the $1,349 Wegovy list price. The deal also extends Medicare coverage of Wegovy for obesity for the first time. In exchange, Novo Nordisk received a three-year exemption from the pharmaceutical tariffs the administration announced, tariffs that would otherwise apply at 100% to patented drugs imported without a Most Favored Nation (MFN) pricing agreement. Given that Novo Nordisk manufactures substantially in Denmark and Europe, the tariff exemption through approximately 2028 is valuable insurance during the period when its US manufacturing buildout is still coming online.

Management expects a negative low-single-digit impact on global sales growth in 2026 from the pricing agreement. That is a real near-term headwind. The medium-term logic is that lower prices plus expanded Medicare access could ultimately drive higher volumes that more than offset the per-unit reduction. I believe that logic is sound, but it will take time to play out.

10. Valuation

What the Market is Pricing in, and What I Think it is Missing

My valuation framework for Bearhold Research expresses intrinsic value as a number of years of embedded discounted cash flows. Rather than using a terminal value, which requires assumptions about perpetuity growth rates that I find too speculative to be reliable, I model an explicit series of annual free cash flows, discount each one back to the present, and ask a simple question: how many years of future cash flows does today’s price already contain? The answer tells me whether I am paying a fair price, a cheap price, or an expensive one.

The framework has five zones. Exceptionally Attractive sits below 15 years. Attractive runs from 16 to 20 years. Hold covers 21 to 30 years. Expensive runs from 31 to 35 years. Exceptionally Expensive is anything above 36 years. I initiate new positions only in the Attractive or Exceptionally Attractive zones and add most aggressively when a business I understand well enters Exceptionally Attractive territory. I sell when a position reaches Expensive or Exceptionally Expensive and reallocate to Attractive names in the Bearhold Universe.

17 Years — Attractive Zone

At $37.50 per share, Novo Nordisk sits at around 17 years of embedded cash flows, firmly in the Attractive zone of the Bearhold framework.

The most important thing to understand about this number is what it does and does not assume. It does not assume a flawless recovery. It explicitly accounts for the near-term FCF (free cash flow) compression driven by the capex cycle, modelling the gradual normalisation as the manufacturing buildout matures rather than assuming an immediate return to historical cash generation levels. It applies a growth rate that is a meaningful haircut to the company’s historical FCF per share CAGR, acknowledging competitive pressure from Lilly in the injectable market, gross margin headwinds from the TrumpRx pricing deal, and patent expiries in China. And it uses a discount rate at the conservative end of the reasonable range for a business of this quality, reflecting the genuine operational uncertainty of this particular moment.

In other words, 17 years is not an optimistic number dressed up as a conservative one. It is what the arithmetic produces when you take the near-term headwinds seriously.

At 17 years, the thesis requires the capex cycle to normalise broadly on schedule, revenue to recover from the 2026 transition year, and FCF per share to compound at a rate that reflects the underlying quality of the franchise rather than the distortions of the current investment cycle. If those things happen, and I believe they will, for reasons I have set out throughout this report, then 17 years represents a genuine margin of safety in a business whose quality justifies a much higher price.

Growth Engines

I evaluate the return potential of any business through two engines running simultaneously.

The first engine is FCF per share growth, the fundamental driver of intrinsic value over time. For Novo Nordisk, the near-term FCF figure is distorted by the capex cycle, and as that distortion clears over the next two to three years, FCF per share growth should re-converge with the underlying earnings power of the franchise. The combination of revenue growth, operating leverage, and a consistent share buyback programme, which has reduced the diluted share count from 5,155 million in FY2015 to 4,448 million in FY2025, provides a quiet compounding mechanism that operates in the background of every other assumption in the model. Even modest share count reduction adds to per share growth without requiring any improvement in the absolute cash generation of the business.

The second engine is valuation re-rating. At 17 years in the Attractive zone, this engine is working in the investor’s favour. The real optionality lies in the scenario where execution delivers, CagriSema approved, capex cycle matures, gross margins recover, oral market share consolidates in Novo Nordisk’s favour, and the market re-rates the stock from Attractive back toward the upper end of Hold or beyond. In that scenario, the investor earns the fundamental compounding of FCF per share growth and a valuation multiple expansion simultaneously. That combination is what makes the Attractive zone entry compelling for a long-term investor

11. Risks

Every investment thesis has a version of events where it is wrong. I want to walk through the scenarios that would genuinely change my view on Novo Nordisk, not the boilerplate risks that appear in every pharmaceutical analysis, but the specific dynamics that keep me thinking carefully about this position.

The Gross Margin is the Number I Watch Most Closely

This is not the risk that gets the most attention, but it is the one I consider most important to the long-term thesis. Novo Nordisk’s gross margin fell from a decade average of approximately 83.9% to 81.0% in FY2025. The official explanation is a combination of rapid manufacturing scale-up costs, one-off restructuring charges, and the initial inefficiency of newly commissioned facilities. If that explanation is correct, gross margins normalise as the new capacity reaches full utilisation over the next two to three years, and the underlying earnings power of the business is largely intact.

But there is an alternative explanation that I cannot dismiss. The TrumpRx pricing deal reduced Wegovy and Ozempic prices to $350 per month on government channels. Competitive pressure in the oral market is pushing both Novo Nordisk and Lilly toward $149 starting prices for their pills. Biosimilar competition is coming in China and eventually in Western markets as patents expire. If these pricing pressures are structural rather than temporary, the long-term gross margin of this business may settle permanently lower than its historical range. A business that earns 79% gross margins rather than 84% is still exceptional, but the difference compounds significantly over a decade of growth at this scale. I do not think this is the most likely outcome, but it is a risk I watch carefully.

The Capex Cycle

Novo Nordisk is spending DKK 60 billion per year, approximately $9 billion, on capital expenditure, and has committed approximately USD 5.6 billion in additional US manufacturing investment through 2028. The total committed capital across the current buildout cycle runs into the tens of billions of dollars. This infrastructure is being built on the assumption that GLP-1 demand will continue to grow rapidly for years and that Novo Nordisk will capture a meaningful share of that growth.

The risk is not that demand for GLP-1 drugs disappoints in aggregate. I believe the structural demand case is overwhelming, as I discussed in the market view section. The risk is more specific: that Novo Nordisk’s share of that demand disappoints relative to the assumptions embedded in the capex decisions. If Lilly continues to gain injectable market share at Novo Nordisk’s expense, and if the oral market develops more slowly than projected, then the company will have built manufacturing capacity for volumes it cannot fill. Capital expenditure is largely irreversible. Factories cannot be unbuilt. The financial consequence would be years of elevated depreciation charges on underutilised assets, compressing returns on invested capital precisely when the business needs to demonstrate that the investment cycle is paying off.

I think this risk is manageable but it is not theoretical. Management made their capacity decisions when Novo Nordisk’s growth trajectory looked dramatically more positive than it does today. The FY2025 full-year sales growth of 10.3% at constant exchange rates versus the FY2026 guidance of negative adjusted sales growth represents a sharp deceleration. How much of that deceleration is transitional, compounding headwinds, pricing adjustments, China patent expiry, and how much of it represents a more durable slowdown in the underlying franchise, will determine whether the capex cycle was visionary or premature.

China Patent Expiry

All of Novo Nordisk’s core semaglutide products have their active ingredient patents expiring in China in 2026. Ozempic, Wegovy, Rybelsus, the entire franchise. China generated DKK 18.7 billion in FY2025 sales and was growing at 5% at constant exchange rates. Novo Nordisk’s Wegovy launch in China has barely begun, with only DKK 796 million in FY2025 revenue, meaning the obesity opportunity there is largely untapped at the moment the moat is about to be breached.

The practical impact will not be immediate. Biosimilar manufacturers need time to build commercial scale, achieve regulatory approvals, and establish distribution networks. Novo Nordisk’s brand recognition, safety data, and clinical relationships provide a buffer. But Chinese pharmaceutical companies are sophisticated, well-capitalised, and experienced in bringing biosimilars to market quickly. Several domestic companies were already preparing semaglutide biosimilars well before the patent expiry. The pricing pressure in China over the next two to three years will be significant, and the obesity market, which was supposed to be a major long-term growth driver in the world’s most populous country, will develop in a far more competitive and lower-margin environment than the one that drove the Western growth story.

The Injectable Efficacy Gap

Tirzepatide’s approximately 21% average weight loss versus semaglutide’s 15% is a real clinical difference that is influencing prescribing behaviour. Novo Nordisk held approximately 59.6% of global branded GLP-1 volume market share in FY2025, but the US prescription trend, Lilly at 57% of monthly prescriptions and rising versus Novo at 43% and falling, is the more relevant near-term signal. The direction matters as much as the level.

The honest risk here is timing. CagriSema, which matches tirzepatide’s efficacy at 22.7% weight loss, is filed for FDA approval with a decision expected around October 2026. If the approval is delayed, through an unexpected complete response letter, additional data requests, or manufacturing inspection issues, Novo Nordisk remains in the gap year for longer than projected. Every additional month without CagriSema is another month of injectable market share drifting toward Lilly, another month of compounders and prescribers defaulting to tirzepatide for new obesity patients, and another month of the narrative calcifying around Lilly as the dominant player. The business does not collapse in this scenario, but the re-rating catalyst is deferred and the share count of prescribers who have built tirzepatide habits grows.

Real-world GLP-1 Adherence, The Recurring Revenue Moat May be More Fragile Than it Appears

I described the recurring revenue nature of GLP-1 drugs as a feature of the moat, patients who stay on therapy for life generate predictable, growing cash flows. The critical assumption is that patients actually stay on therapy. The real-world data on this is sobering. First-year discontinuation rates for injectable GLP-1 drugs in real-world settings have been estimated at 40 to 50% in multiple analyses, significantly higher than the dropout rates observed in tightly controlled clinical trials.

The reasons are well-documented: gastrointestinal side effects concentrated in the dose-escalation phase, cost and coverage barriers, weight loss plateaus that disappoint patients expecting linear progress, and the practical difficulty of managing a weekly injection in daily life over years. If a meaningful share of the patients who started on Wegovy or Ozempic in the 2022 to 2024 wave have already discontinued, the installed base of recurring prescriptions is smaller than the volume data implies, and the forward revenue from that cohort is lower than a pure adherence model would project.

This dynamic also has a second-order implication for the capex cycle. If real-world adherence is significantly worse than clinical trial data suggests, the demand projections management used when authorising DKK 60 billion annual capital expenditure may have been built on an assumption that the treated population compounds reliably over time. If the population turns over faster, patients starting, stopping, and restarting, the demand profile becomes more volatile and harder to forecast accurately.

The Diabetes-obesity Paradox, long-term Structural Uncertainty

I discussed this in section 3 as a paradox rather than a risk, but at a multi-decade horizon it becomes one. If GLP-1 obesity drugs achieve the penetration rates the most optimistic projections envision, treating hundreds of millions of people globally over the next twenty years, the downstream effect on type 2 diabetes incidence will be measurable. The patients who avoid diabetes because of sustained GLP-1 treatment are patients who do not eventually need insulin, metformin, and diabetes-specific medications. Novo Nordisk’s diabetes franchise, still generating DKK 207 billion in FY2025, by far the larger segment, will face a structurally shrinking addressable market over a long enough time horizon.

I do not think this plays out as a crisis. The transition will be gradual, the diabetes franchise will continue generating strong cash flows for many years, and the obesity revenue replacing it operates at similarly high margins. But any honest long-range model for this business needs to account for the possibility that the company’s most important product is, over a long enough horizon, cannibalising the market for its second most important product line. The net effect is probably positive, obesity revenue grows faster than diabetes revenue declines, but the uncertainty is real and deserves acknowledgment.

The Verdict

Bearhold Universe Status: Watchlist

The Approved designation in the Bearhold Universe is purely qualitative. It has nothing to do with valuation, price, or near-term earnings visibility. It asks one question: has this business demonstrated, through a sufficient track record, that it can sustain excellence in its competitive arena the way the best businesses in history have? The answer determines the designation. The price determines when I act.

Novo Nordisk’s insulin franchise answers that question without hesitation, and I want to be clear about why. This is not a business that stumbled into a good decade. It is a business that built a durable competitive position over a century, through two world wars, through the transition from animal insulin to recombinant DNA technology, through the commoditisation of older molecules, through the arrival of new drug classes that threatened its core. In every one of those transitions, Novo Nordisk did not just survive. It adapted, invested, and emerged with a stronger position than it entered with. The operating margin holding between 41% and 46% across every single year from 2015 to 2025, through a global pandemic, a complete revenue mix transformation, and a manufacturing buildout of historic proportions, is the financial expression of a century of that institutional resilience. The insulin franchise is Approved, unambiguously and permanently.

The obesity franchise is where I have to be honest about what I know and what I do not yet know. And the distinction matters enormously to me, because the Approved designation is a statement about demonstrated quality, not about the quality I believe is coming.

What I know is this. Semaglutide’s clinical evidence base is exceptional. The SELECT trial reducing major adverse cardiac events by 20% in people with established cardiovascular disease. The FLOW trial reducing chronic kidney disease progression by 24%. The STEP trials producing average weight loss of 14.9%, extraordinary by any historical standard in obesity pharmacology. These are not marginal results. They are practice-changing outcomes that have permanently altered clinical guidelines across cardiology, nephrology, and obesity medicine simultaneously. The commercial execution behind these results has been equally impressive. DKK 82 billion in obesity care revenue in FY2025 from essentially nothing six years ago, with a global manufacturing buildout that represents the largest capital commitment in the company’s history. Management made the right strategic bet, made it early, and executed it at scale.

What I do not yet know is whether Novo Nordisk will dominate the obesity market the way it dominated the insulin market. And that distinction is exactly where the Watchlist designation lives.

Eli Lilly’s tirzepatide currently demonstrates superior injectable efficacy, approximately 21% average weight loss versus semaglutide’s 15% in their respective pivotal trials. That gap is real and it is influencing prescribing behaviour in measurable ways. By the third quarter of 2025, Lilly held more than 57% of US monthly GLP-1 prescriptions, having overtaken Novo Nordisk from a position of no market presence just three years earlier. That is a competitive trajectory that deserves honest acknowledgment. Novo Nordisk pioneered this market and is currently being challenged within it by a competitor with a better efficacy number in the most commercially important indication.

CagriSema is Novo Nordisk’s answer. Filed with the FDA in December 2025 with a decision expected around October 2026, it produced 22.7% weight loss in the REDEFINE 1 trial, essentially matching tirzepatide’s headline figure and doing so with a novel dual-mechanism approach combining semaglutide with a long-acting amylin analogue. If CagriSema is approved and demonstrates competitive real-world efficacy, it closes the injectable gap before Lilly’s next-generation retatrutide reaches market. The pipeline response is credible. But it is a promise, not yet a result. And the Approved designation requires results.

The oral market is equally unresolved. On April 1, 2026, twelve days before this report was published, the FDA approved Eli Lilly’s orforglipron, now branded Foundayo, as the second oral GLP-1 pill for obesity. The ORION indirect comparison data, presented the following day, suggests the Wegovy pill has meaningful advantages in both efficacy and tolerability. Patients on orforglipron showed approximately four times higher odds of discontinuing due to adverse events and nearly fourteen times higher odds of discontinuing specifically due to gastrointestinal side effects. These are striking numbers and they support a compelling narrative for the Wegovy pill’s commercial position. But this is an indirect comparison across separate trials, funded and presented by Novo Nordisk, with wide confidence intervals and no head-to-head trial to settle the question definitively. The oral market battle between these two drugs will play out in real prescriptions over the next twelve to eighteen months, and those real-world results are what the quality assessment requires, not an indirect comparison published the day after a competitor’s approval.

This is what the Watchlist is designed to capture. The insulin franchise is proven. The obesity franchise is promising, credibly positioned, and backed by a pipeline that could decisively establish Novo Nordisk’s leadership in the new competitive arena. But the competitive outcome has not yet been determined. The prescription share trajectory, the CagriSema approval and launch, and the oral market real-world data will together tell the story that the insulin franchise told over decades, except compressed into the next two to three years because the competitive intensity demands it.

The specific triggers that would move Novo Nordisk from Watchlist to Approved are these. CagriSema receiving FDA approval and demonstrating competitive or superior real-world efficacy versus tirzepatide in its first year of commercial prescription data. And the oral market prescription trends confirming over at least two to three quarters that the Wegovy pill’s tolerability advantage holds in actual patient behaviour, that patients are staying on it longer and discontinuing less than Foundayo in the real world, not just in an indirect trial comparison. When those two conditions are met, the obesity franchise will have earned the track record the designation requires. It will have demonstrated that Novo Nordisk can do in obesity what it did in insulin, build a leadership position and defend it against serious competition through product quality, not just first-mover advantage.

At $37.50 and 17 years of embedded cash flows, the price sits in the Attractive zone of the Bearhold valuation framework. The business I have described in this report is exceptional. The near-term headwinds, negative 2026 guidance, China patent expiry, the capex cycle compressing free cash flow, the CEO transition, are all real and all visible in the numbers. None of them concern me as a long-term investor. What keeps Novo Nordisk on the Watchlist rather than in the Approved column is not weakness. It is the honest acknowledgment that the most important competitive chapter of this company’s modern history is being written right now, in real time, with the outcome still genuinely uncertain. I will be watching that chapter closely. And when the evidence confirms what the insulin franchise already demonstrated about this company’s ability to build and defend category leadership, the designation will change.

This report reflects the author’s personal views and does not constitute investment advice. Investing carries the risk of permanent capital loss. The author held a position in NVO during the research process and exited prior to publication. No position is held at the time of publishing. Read the full disclaimer here

Sources:

Novo Nordisk Annual Report FY2025 (DKK)

Novo Nordisk Annual Report FY2024;

FDA Declaratory Order on semaglutide shortage, February 21, 2025;

Novo Nordisk NDA filing for CagriSema, December 18, 2025; REDEFINE 1 and REDEFINE 2 Phase 3 trial data;

SELECT cardiovascular outcomes trial;

FLOW kidney disease trial;

ORION indirect treatment comparison, Obesity Medicine Association 2026, April 10–12, San Diego;

OPTIC patient preference study, Novo Nordisk, October–November 2025;

FDA approval of Foundayo (orforglipron), April 1, 2026;

White House TrumpRx / MFN pricing announcement, November 2025;

Trump Administration pharmaceutical tariff Executive Order, April 2026;

Morningstar GLP-1 market analysis, December 2025;

J.P. Morgan GLP-1 market projections, 2026.